Echelon Financial Holdings Inc. sees lower net income for 2016 full-year, Q4 over prior-year periods

February 17, 2017 by Canadian Underwriter

Print this page Share

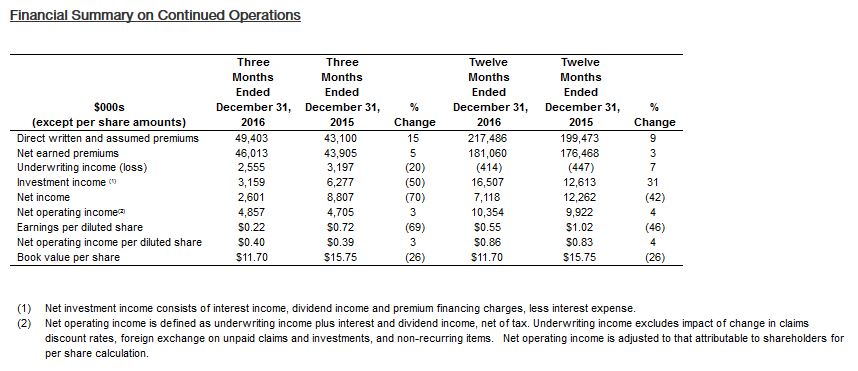

It was a mixed bag for Echelon Financial Holdings Inc. (EFH) in the fourth quarter of 2016, with strong commercial lines results and lower personal lines results combining to contribute to a 70% drop in net income to about $2.6 million compared to 2015 Q4.

Specifically, net income in 2016 Q4 was approximately $2.6 million compared to $8.8 million for 2015 Q4, note figures in a statement issued late Thursday by EFH.

Specifically, net income in 2016 Q4 was approximately $2.6 million compared to $8.8 million for 2015 Q4, note figures in a statement issued late Thursday by EFH.

The company, whose Canadian subsidiary is Echelon Insurance, operates in the property and casualty insurance industry in Canada, primarily focusing on non-standard automobile insurance and other specialty p&c insurance products.

There was also a decrease for full-year 2016, although not as severe. Net income for the 12 months ended Dec. 31, 2016 was $7.1 million, down 42% compared to approximately $12.3 million for the same period of 2015.

The story for net operating income – underwriting income plus interest and dividend income, net of tax – was more positive for both full-year and fourth quarter 2016.

Net operating income was up 3% to about $4.9 million in 2016 Q4 compared to $4.7 million in 2015 Q4. For the full-year period, net operating income was $10.3 million in 2016 compared to $9.9 million in 2015, an increase of 4%.

Both direct written and assumed premiums (DWP) and net earned premiums (NEP) were also up for both fourth quarter and full-year compared to the prior-year periods.

DWP amounted to $49.4 million in 2016 Q4, up 15% compared to $43.1 million in 2015 Q4, primarily driven by additional new products across Canada; NEP was up 5% to $46.0 million from $43.9 million.

For the full-year periods, DWP was 9% higher at about $217.5 million in 2016 – attributable predominantly to new product lines in surety and commercial auto and stronger broker relationships – compared to approximately $199.5 million in 2015.

NEP, for its part, was up 3% to about $181.1 million from about $176.5 million, the company notes.

With regard to underwriting results, income was down 20% to about $2.6 million in the fourth quarter of 2016 compared to about $3.2 million in the same quarter of 2015.

For full-year, EFH posted a 7% improvement, but still a $414,000 loss in 2016 compared to an underwriting loss of $447,000 in 2015.

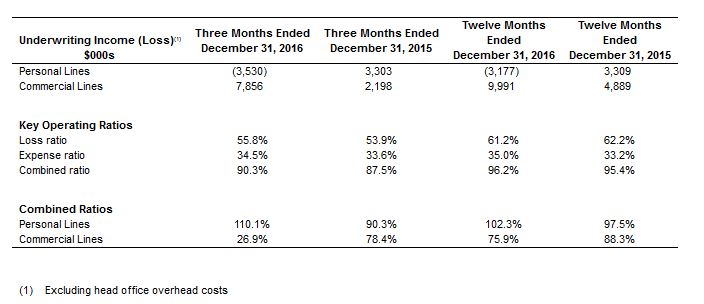

Looking by line, EFH reports personal lines generated an underwriting loss of $3.5 million in 2016 Q4 compared to an underwriting income of $3.3 million in 2015 Q4, “primarily due to weak performance in Ontario auto driven by increased severity in claims.”

Looking by line, EFH reports personal lines generated an underwriting loss of $3.5 million in 2016 Q4 compared to an underwriting income of $3.3 million in 2015 Q4, “primarily due to weak performance in Ontario auto driven by increased severity in claims.”

For commercial lines, underwriting income of $7.9 million in the fourth quarter of 2016 compared to $2.2 million in the same period of 2015, “due to strong performance across Canada,” the release notes.

“The company continues to focus on growing the Canadian business through product expansion, investments in technology and strong broker relationships,” it adds.

For all of 2016, personal lines generated an underwriting loss of $3.2 million compared to an underwriting income of $3.3 million in 2015.

Commercial lines generated an underwriting income of $10.0 million in 2016 compared to $4.9 million in 2015 “due to strong performance of property and liability, warranty and commercial auto products,” the company states.

A Canadian combined operating ratio of 90% in the fourth quarter of 2016 compared to 88% in the prior-year quarter, EFH reports. “Our fourth quarter results were mixed,” says EFH CEO Serge Lavoie.

“We were very pleased by the exceptional results reported in commercial lines across the country. However, our personal lines performance was negatively impacted by increased claims severity in Ontario auto, in line with market experience,” Lavoie notes.

“Most of these claims were reported prior to the introduction of the June 2016 reforms, which we hope will reduce catastrophic claims moving forward. We will continue to monitor our claims closely,” he continues.

EFH previously announced it is exiting the European market to focus on growing its Canadian operations.

Related: Echelon Financial Holdings Inc. sees lower net income in 2016 Q2, will focus on Canadian operations

It was noted in a statement last August that the company has entered into a definitive stock purchase agreement to sell its European insurance operations, “allowing us to allocate our capital to grow the Canadian operations,” Lavoie said at the time.

“We are currently awaiting approval for the change of control application submitted to the Danish Financial Services authority for the divestiture of the European operations,” the company statement Thursday adds.

Reports Lavoie, “Our expectation is that we will have a decision within the next two or three weeks.”

Other company results include the following:

- investment income in 2016 Q4 was $3.2 million compared to $6.3 million in 2015 Q4, primarily as a result of lower preferred shares mark-to-market gains compared to the prior-year period;

- the fair value of the investment portfolio, including finance receivables, was $410 million in 2016 Q4;

- total pre-tax loss on invested assets of $0.6 million in 2016 Q4 compared to a pre-tax gain of $6.2 million in 2015 Q4, largely due to higher government bond yields and lower gains on Preferred Shares compared to prior-year quarter;

- net income attributable to shareholders on continued operations was $2.6 million, or $0.22 per diluted share, for 2016 Q4; and

- the Minimum Capital Test (MCT) ratio of Echelon Insurance at Dec. 31, 2016 was 237%, which exceeds the supervisory regulatory capital level required by the Office of the Superintendent of Financial Institutions.

Pointing out the company has made meaningful progress on its strategy, Lavoie reports improvements have been made to personal lines operations and strong teams have been assembled to support the surety, commercial auto and commercial property products.

“These expanded business lines have been very well-received by existing and new brokers, and we look forward to continuing to build and develop our relationships with them,” he says.

“We are also scheduled to roll out our policy management system to the majority of our brokers in Ontario, Quebec and Alberta in the next few weeks, which will greatly improve our ability to transact seamlessly with them,” Lavoie adds.

Have your say: