Combined ratio, net loss for Economical Insurance up in 2017 Q3 over 2016 Q3

November 6, 2017 by Canadian Underwriter

Print this page Share

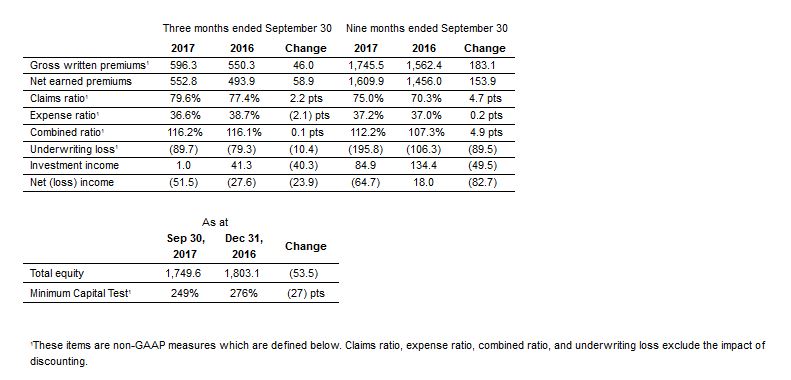

The impact of strategic investments by Economical Insurance contributed to the insurer witnessing a combined ratio of 116.2% and an almost doubling of net loss in 2017 Q3 compared to 2016 Q3.

The combined ratio for the third quarter of 2017 includes “an impact of 8.1 percentage points related to strategic investments in our personal lines business,” notes a statement from the Waterloo, Ont.-based p&c insurer that services 1 million-plus customers country-wide and had $2.2 billion in annualized premium volume as at Sept. 30, 2017.

The combined ratio for the third quarter of 2017 includes “an impact of 8.1 percentage points related to strategic investments in our personal lines business,” notes a statement from the Waterloo, Ont.-based p&c insurer that services 1 million-plus customers country-wide and had $2.2 billion in annualized premium volume as at Sept. 30, 2017.

Economical Insurance’s net loss for the third quarter of 2017 amounted to $51.5 million compared to a loss of $27.6 million in the prior-year quarter, the company reported Friday in releasing its consolidated financial results

For the first nine months of 2017, Economical Insurance went from net income of $18 million in 2016 to a net loss of $64.7 million in 2017.

For both the third quarter and year to date, the net loss was “primarily due to a combination of lower investment income and higher underwriting losses.”

Rowan Saunders, President and CEO of Economical Insurance

The Q3 results “continue to reflect the trends we experienced in the first half of the year. Gross written premiums (GWP) continued to grow, driven by personal lines. However, the pace of growth slowed due to the effects of our corrective underwriting and pricing actions,” Rowan Saunders (pictured right), president and CEO of Economical Insurance, explains in the company statement.

The underwriting loss for 2017 Q3, again, worsened in the third quarter of 2017 compared to the prior-year quarter loss, settling at $89.7 million compared to $79.3 million.

The negative change was more pronounced when results for the first nine months of the year are considered. Underwriting loss for the period in 2017 was $195.8 million compared to $106.3 million for the same nine months of 2016.

Overall, commercial lines produced an underwriting loss of $36.5 million in the third quarter of 2017 compared to $21.8 million in the same quarter a year ago. While premiums were again on the rise, challenges remain, particularly with respect to commercial lines.

Overall, growth in personal lines drove total GWP up by 8.4%, increasing to $596.3 million in 2017 Q3 compared to $550.3 million in 2016 Q3. Comparing the two periods, net earned premiums (NEP) also rose to $552.8 million compared to $493.9 million.

GWP and NEP were up for the first three quarters of 2107 compared to 2016, amounting to about $1.7 billion and $1.6 billion, respectively.

By line, however, the story was different. Personal lines GWP grew by $57.5 million or 15.8%, driven by increased auto and property policy volumes in the broker channel, new business growth from the direct distribution channel Sonnet, and the acquisition of Petline.

Related: Economical Insurance completes acquisition of Canada’s largest pet insurer

Compare that to commercial lines, where GWP declined by $11.5 million or 6.1%.

The decrease was as a result of “the implementation of our targeted pricing, underwriting and broker management actions began to take hold. We expect continued downward pressure on the commercial lines GWP as our planned actions continue to be implemented over the upcoming quarters,” Economical Insurance reports.

Year-to-date in 2017, personal lines premiums grew by 18.2% and commercial lines premiums grew 0.5% compared to the same nine months of 2016.

Challenges with commercial lines have already elicited corrective actions, with more anticipated by the end of the year. In 2017 Q2, Economical Insurance initiated a comprehensive review of its commercial line portfolio by region and product type.

“This ongoing review has led to a number of actions in the second and third quarters, including exiting unprofitable books of business and certain product offerings, targeted rate increases, and increased underwriting discipline,” the statement reports.

“These actions have impacted our policy volumes and gross written premiums during the quarter, and this is expected to continue as further actions are implemented from our review. This should result in a more favourable mix of commercial business and improve operating performance going forward,” the insurer points out.

“The performance of our auto lines, and, in particular, commercial fleet business, continues to be challenged,” Saunders points out.

“Auto lines remain challenged, primarily in Ontario, Alberta and British Columbia. We have implemented targeted pricing and underwriting actions in all three regions during the year,” the press release adds.

For personal auto, the improved combined ratio for the third quarter of 2017 compared to the same quarter of 2016 was “primarily due to lower levels of catastrophe losses. The same quarter a year ago was impacted by a number of wind, hail and rain storms in Alberta,” the statement notes.

For personal property, again the adjusted personal property combined ratio improved “due to lower levels of weather-related catastrophe losses. The current quarter was primarily impacted by the British Columbia wildfires and the Windsor flood, whereas the same quarter a year ago was impacted by a number of wind, hail and rain storms in Alberta,” it explains.

The overall combined ratio for 2017 Q3 – impacted 8.1 percentage points in 2017 Q3 compared to 7.7 percentage points in 2016 Q3 – has been affected by the insurer’s continuing significant investments in Sonnet and replacement of its policy administration system, primarily for personal lines broker business.

Related: ‘Clock is running’ as Economical Insurance prepares for public offering: Saunders

“We expect that these strategic investments will impact our underwriting results during the ongoing implementation and start-up phases, but are expected to improve our long-term profitability,” the insurer adds.

To address remaining challenges, Saunders notes, “we will be implementing further actions by the end of the year, but they will take time to earn through our results.”

Have your say: