Echelon Insurance reports near halving of net income in 2017 Q3 compared to 2016 Q3

November 3, 2017 by Canadian Underwriter

Print this page Share

The B.C. wildfires and losses related to commercial auto and motorcycle contributed to Echelon Insurance witnessing a 42% decrease in net income and an increase in combined operating ratio for 2017 Q3 compared to 2016 Q3.

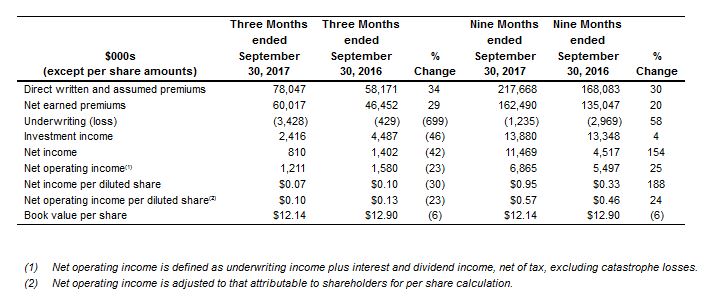

Net income amounted to $810,000 for the quarter ending Sept. 30, 2017 compared to $1.4 million for the prior-year quarter, notes a statement Thursday from Echelon Financial Holdings Inc.

Net income amounted to $810,000 for the quarter ending Sept. 30, 2017 compared to $1.4 million for the prior-year quarter, notes a statement Thursday from Echelon Financial Holdings Inc.

But net income for the first nine months of 2017 was up considerably year over year, reaching $11.5 million in 2017 compared to $4.5 million in 2016, reports Echelon Insurance, which operates in Canada’s p&c insurance industry and provides personal and commercial lines insurance exclusively through the broker channel.

With regard to net operating income on continued operations for the third quarter of 2017, that, too, was down compared to the same quarter of 2016. In 2017 Q3, it was $1.2 million, down 23% from the approximately $1.6 million in 2016 Q3.

With regard to net operating income on continued operations for the third quarter of 2017, that, too, was down compared to the same quarter of 2016. In 2017 Q3, it was $1.2 million, down 23% from the approximately $1.6 million in 2016 Q3.

For the first three quarters of 2017, net operating income on continued operations increased 25% to $6.9 million from $5.5 million.

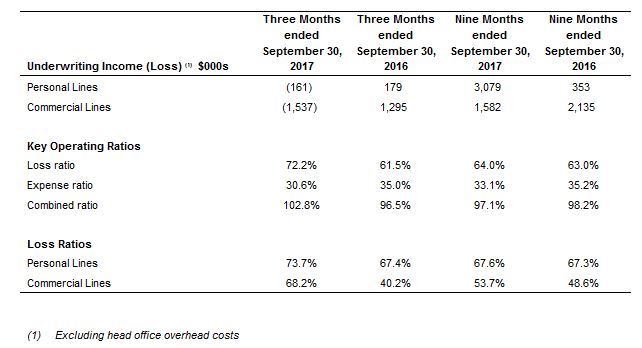

With regard to the company’s combined operating ratio, it climbed to 103% in the third quarter of 2017 compared to 97% in the third quarter of 2016.

The change was “driven by the impact of the B.C. wildfires, one large loss in Commercial Auto, and increased Motorcycle claims due to unusually dry late summer weather experienced in Ontario,” the company explains.

Excluding the impact of the wildfires, the combined operating ratio for 2017 Q3 would have still increased, but less so, reaching 99.5%.

Citing the wildfire, commercial auto loss and motorcycle losses, Serge Lavoie, CEO of Echelon Insurance, emphasizes “we remain committed to supporting our customers who have experienced losses in B.C., and across the country.”

Citing the wildfire, commercial auto loss and motorcycle losses, Serge Lavoie, CEO of Echelon Insurance, emphasizes “we remain committed to supporting our customers who have experienced losses in B.C., and across the country.”

The company’s underwriting loss in 2017 Q3 increased almost seven times over the prior-year period, amounting to $3.4 million compared to $429,000.

For the first nine months of 2017, however, the underwriting loss went down compared to the same period in 2016. In 2017, it was $1.2 million compared to just shy of $3.0 million in 2017.

By line, Personal generated an underwriting loss of $0.2 million in 2017 Q3 compared to an underwriting income of $0.2 million in 2016 Q3 as a result of “a $2.0 million adverse impact from the wildfires in British Columbia, in addition to an unusual number of large losses in the Motorcycle line of business.”

For Commercial, this accounted for an underwriting loss of $1.5 million in the third quarter of 2017 compared to an underwriting income of $1.3 million in the prior-year quarter. This decreased, the company reports, was “driven by one large loss in Commercial Auto.”

For the first nine months of 2017, Personal “generated underwriting income of $3.1 million compared to an underwriting income of $0.4 million in the same period last year, primarily due to strong performance in Ontario and Quebec auto,” it notes.

For Commercial, underwriting income amounted to $1.6 million in 2107 Q3 compared to $2.1 million in 2016 Q3, “predominantly due to one large loss in commercial auto,” Echelon Insurance reports.

On the premium front, both direct written and assumed premiums and net earned premiums (NEP) for the company increased in the third quarter of 2017 compared to the third quarter of 2016.

Direct written premiums increased 34% to $78.0 million in 2017 Q3 compared to $58.2 million in 2016 Q3, while NEP was up 29% to $60.0 million compared to $46.5 million. For the nine months ended Sept. 30, direct written premiums were up 30% and NEP was up 20%.

“Net favourable development of prior-year claims of $12.3 million was recorded in the third quarter of 2017 compared to net favourable development of $4.5 million in the same period in 2016 driven by better than expected development of prior-year claims, particularly in Personal Lines, in addition to an increase in discount rate,” the company statement explains.

The 34% increase in direct written premiums during 2017 Q3 was “as a result of organic growth in Personal Lines and new Commercial Lines products launched in 2016,” Echelon Insurance points out.

Serge Lavoie, Chief Executive Officer or Echelon Insurance

With regard to investment income, this amounted to $2.4 million in the third quarter of 2017 compared to $4.5 million in the third quarter of 2016.

“The pre-tax loss on invested assets was $1.0 million in the quarter, negatively impacted by lower returns on the fixed income portfolio due to increased underlying government bond yields in the quarter, compared to a pre-tax gain of $3.7 million in the third quarter of 2016,” the company statement explains.

“We continue to execute on our broker-focused strategy, which has been well-received by brokers across the country,” Lavoie (pictured left) says in the statement.

“We have also made good progress in the deployment of our new policy management system leading to improved broker connectivity and customer service in the future,” he adds.

Related: Non-standard auto insurer Echelon completes sale of European operations

Have your say: