Recent quakes a reminder of the importance of insurance options in U.S.: III

April 19, 2016 by Canadian Underwriter

Print this page Share

Many states in the United States face risks from earthquakes, yet only about 10% of surveyed homeowners on the West Coast have purchased related coverage, reports the Insurance Information Institute (III).

Recent earthquakes in Ecuador and Japan serve as a reminder to consider whether or not having such coverage in place makes sense.

Just last week, a magnitude 7.8 earthquake struck Ecuador, killing at least 272 people and injuring more than 2,500 others, and a magnitude 6.5 quake hit the Kumamoto prefecture of Japan followed about a day later by a magnitude 7.3 quake in the region, III reports. Japanese officials had confirmed 41 deaths at the time.

Related: Second earthquake in two days in Japan causes landslides

“Despite the earthquake threat in many states, including California and the Pacific Northwest, only about one in every 10 residential households on the West Coast have coverage for quake-caused property damage,” notes information included in III’s 2015 Pulse Survey. Specifically, the survey shows 18% of homeowners in the West were most likely to buy earthquake coverage, followed by the Northeast at 9%, the Midwest at 8%, and the South at 7%.

Earthquake-related damage, such as fire and water damage as a result of burst gas and water pipes, is generally provided by standard homeowners and renters insurance policies.

However, protection from the shaking and cracking caused by earthquakes that can destroy buildings and personal possessions is not covered under standard homeowners or business insurance policies, the institute notes. Rather, it is “generally available in the form of a supplemental policy.”

As for cars and other vehicles, III adds that these are covered for earthquake damage under the optional comprehensive portion of an auto insurance policy.

Insurers in states with a higher than average risk of earthquakes – such as Washington, Nevada and Utah – often set minimum deductibles at about 10% (so equal to $10,000 on a home that would cost $100,000 to rebuild completely).

“In most cases, consumers can get even higher deductibles to save money on earthquake premiums,” III explains. [click image below to enlarge]

From 2009 to 2014, sales of earthquake insurance (measured in terms of premiums written) rose by only 4.5% in California compared to 13.2% for the U.S. overall. Oklahoma led the way for coverage with an increase of 242% over this same period of time (294% through 2015), as concern over earthquake damage from fracking activity became more widespread, the statement notes.

The institute notes that earthquake insurance rose from US$2.7 billion in 2013 to US$2.8 billion in 2014. “California had the largest amount of earthquake premiums in 2014, at US$1.7 billion, accounting for 59% of U.S. earthquake insurance premiums written,” III notes in a backgrounder. “This figure includes the state-run California Earthquake Authority, the largest provider of earthquake insurance in California,” the backgrounder adds.

III reports that in 2015, seismicity continued to rise in the central U.S., with 32 earthquakes of magnitude 4.0 and greater in states such as Kansas, Oklahoma and Texas. This total compared with 17 such earthquakes in 2014.

“While we’re seeing an increase in earthquake coverage in the most vulnerable states, everyone – no matter where they live – should contact their insurance professional to make sure that they have the right type and amount of insurance,” advises Janet Ruiz, III’s California representative.

In 2015, III cites the U.S. Geological Survey as reporting there were 19 quakes worldwide of magnitude 7.0 or higher. The average has been about 18 such earthquakes per year for over 100 years.

The costliest-ever earthquake in the U.S. was the 1994 Northridge quake, which caused US$15.3 billion in insured damages when it occurred (about US$25 billion in 2015 dollars). It ranks as the fifth-costliest U.S. disaster, based on insured property losses (in 2015 dollars), topped only by Hurricane Katrina, the attacks on the World Trade Center, Hurricane Andrew and Superstorm Sandy.

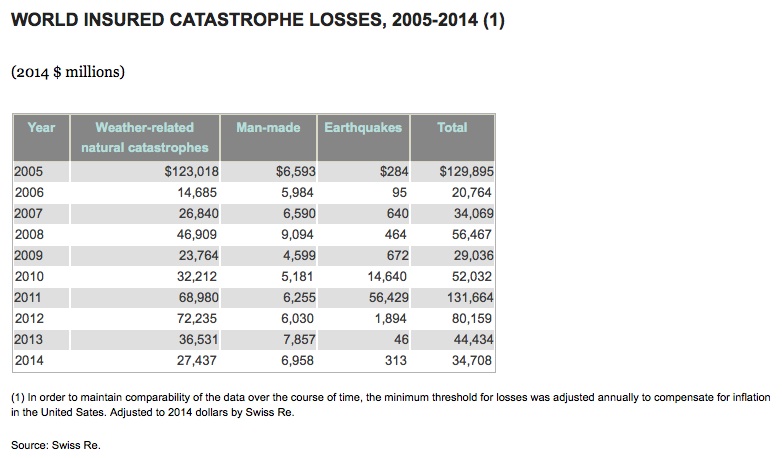

“Insured losses from earthquakes and tsunamis were US$313 million in 2014, higher than the US$45 million in insured losses resulting from earthquakes in 2012, but far below 2011’s record US$54 billion,” III reports in the backgrounder, citing figures from Swiss Re.

Related: ‘Fair amount of uncertainty’ of financial impact of Canadian earthquakes: OSFI deputy superintendent

More recently, Munich Re reports that the 6.0-magnitude earthquake in South Napa, California in Aug. 2014 resulted in US$700 million in total damage and US$150 million in insured losses.

“All Americans need to be financially prepared, and have an up-to-date home inventory and an evacuation plan,” Ruiz emphasizes.

Print this page Share

Apparently, in Canada, we really don’t need to worry at all. According to this article the only earthquake dangers are in the United States. 🙂 (there’s no way that the writer would be so irresponsible as to only cover earthquakes in the US, because those are the only “important” ones. Right?) (A website about Canada would never be so lazy as to just run an American story about earthquakes as boiler plate, without adding – or even knowing if there even was any – Canadian related content, either. Right? Right?!?)