Echelon Financial Holdings Inc. sees lower net income in 2016 Q2, will focus on Canadian operations

August 5, 2016 by Canadian Underwriter

Print this page Share

Echelon Financial Holdings Inc. (EFH) is exiting the European market to focus on growing its Canadian operations, which were negatively affected by the Fort McMurray wildfires that contributed to lower net income for both 2016 H1 and Q2 compared to prior-year periods.

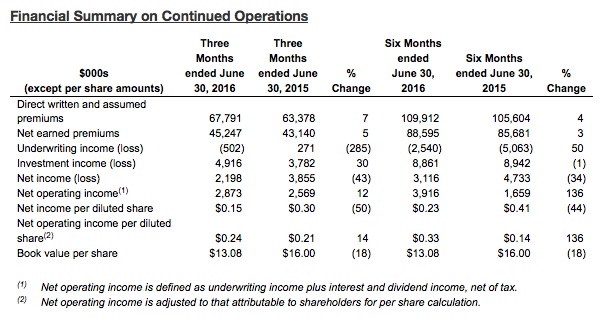

Net income for the three months ended June 30, 2016 fell 43% to about $2.2 million compared to about $3.9 million in the second quarter of 2015, EFH reports in a statement Thursday.

Net income for the three months ended June 30, 2016 fell 43% to about $2.2 million compared to about $3.9 million in the second quarter of 2015, EFH reports in a statement Thursday.

With regard to first-half financial results, the net income for 2016 was down to $3.1 million compared to $4.7 million in 2015, reports the company, which operates in the property and casualty insurance industry in Canada and Europe, focusing on non-standard auto and other specialty p&c insurance products.

But EFH’s net operating income – defined as underwriting income plus interest and dividend income, net of tax – climbed for both 2016 Q2 and H1 periods.

The figures show that net operating income amounted to about $2.9 million in the second quarter of 2016 compared to about $2.6 million in the prior-year quarter, a 12% increase. “The increase was due to improved underwriting income of $1.5 million, excluding the $2 million net impact of the Fort McMurray wildfire,” EFH reports in the statement.

For the first half, net operating income was $3.9 million in 2016, up considerably from about $1.7 million in the same period in 2015. “The increase was due primarily to improved personal lines results in the year.”

Results were also encouraging on the premium front. Direct written and assumed premiums were up 7% to $67.8 million in 2016 Q2 compared to $63.4 million in 2015 Q2, reflecting strong broker relationships and an increase in policies in force in Ontario and Western Canada.

These premiums amounted to $109.9 million in the first half of 2016 – up attributable primarily to increases in personal lines policies – compared to $105.6 million in the same period of 2015.

With regard to net earned premiums (NEP), these increased 5% to $45.2 million in the second quarter of 2016 compared to $43.1 million in the second quarter of 2015. For H1 results, NEP fell slightly to $88.6 million from $85.7 million.

And underwriting income turned to underwriting loss for 2016 Q2 compared to 2015 Q2, with EFH reporting a loss of $502,000 compared to income of $271,000 for the prior-year quarter.

The results were “negatively impacted by losses from Fort McMurray wildfires and a few unusually large auto claims,” the company reports.

Specifically, personal lines generated an underwriting loss of $600,000 in 2016 Q2 compared to an underwriting income of $1.8 million in 2015 Q2. For commercial lines, it generated an underwriting income of $1.6 million in the second quarter of 2016 compared to $300,000 in the same period of 2015, primarily due to favourable development on prior-year claims.

While there was still a loss for the six months ended June 30, 2016, it decreased from the prior-year half. In 2016 H1, EFH saw an underwriting loss of $2.5 million compared to an underwriting loss of $5.1 million in 2015 H1.

The company has entered into a definitive stock purchase agreement to sell its European insurance operations. “We will have exited the European market expeditiously with no residual liabilities, allowing us to allocate our capital to grow the Canadian operations,” says Serge Lavoie, EFH’s chief executive officer.

Serge Lavoie, chief executive officer of Echelon Financial Holdings Inc.

EFH has “completed the build of our surety, commercial auto and commercial property teams in order to offer our brokers a full product suite,” Lavoie (pictured right) reports in the statement.

The idea is to build “a much stronger and sustainable specialty insurance business in Canada directly aligned to the needs of our brokers and clients,” he points out.

Although second quarter results were negatively affected by the Fort McMurray wildfires and a very unusual number of large claims in personal lines, he says, “our Canadian business has produced solid underwriting profits over time and the introduction of new products and enhanced systems will help accelerate growth through 2017 and beyond.”

Other EFH results include the following:

- while the combined ratio was 101% in 2016 Q2 compared to 99% in 2015 Q2, Canadian operations generated a combined ratio of 97.7%;

- a 9% increase in net written premiums on continued operations to $63.5 million in Q2, primarily driven by increased personal lines premiums;

- there was a loss of $2.23 per share on the International operations, consisting of an operating loss of $0.37 per share and a loss on the sale of the business of $1.86 per share;

- total pre-tax gain on invested assets of $5.1 million in 2016 Q2 compared to a pre-tax loss of $1.1 million in 2015 Q2, primarily due to improved performance of the Canadian preferred share portfolio; and

- the minimum capital test (MCT) rato of EFH’s Canadian subsidiary, Echelon Insurance, was 240% as of June 30, 2016.

Print this page Share

Echelon is a very small player in a huge game , dominated by several very big players intending to remain dominating.

For a small player to succeed and exist, they must be satisfied with the “table scraps” of the very big & that is simply an economic fact.

Mr Lavoie’s focus, appears to be moving Echelon into market area’s more compatible to existing expertise. We certainly expect this “focus” to drive the company & allow their continued growth.