Confusion, frustration common to BI claims can be lessened: RIMS survey

April 26, 2017 by Angela Stelmakowich

Print this page Share

PHILADELPHIA – Quantifying business interruption losses continues to be a big challenge, reported by almost six in 10 RIMS members taking part in a recent survey, but a well-conceived approach by risk managers can help to clear any hurdles.

“By taking control of their data, establishing a team and developing plausible BI figures before losses occur, risk managers can do much to lessen the confusion and frustration common to these claims process,” suggests the RIMS Business Interruption Survey 2017, announced Tuesday during the RIMS 2017 Annual Conference and Exhibition.

“By taking control of their data, establishing a team and developing plausible BI figures before losses occur, risk managers can do much to lessen the confusion and frustration common to these claims process,” suggests the RIMS Business Interruption Survey 2017, announced Tuesday during the RIMS 2017 Annual Conference and Exhibition.

“Getting a handle on a BI claim starts well before the event takes place,” states the report. But by adopting the aforementioned approach – and doing it well – “the BI process will be much less burdensome,” it suggests. For the purposes of the report, BI includes time element coverage.

Developed by members of RIMS Business Interruption Working Group, survey findings reflect input from 372 RIMS members who took part in the online poll last fall.

The working group comprised of global BI experts from leading underwriters, accounting firms and brokerages “oversaw the survey, providing analysis and case studies to further explain the findings,” notes a release from RIMS, the risk management society.

A number of key findings from the report, some of which clearly illustrate the reported difficulty surveyed risk managers are having, include the following:

- 58% who have been through a claim said “difficulty quantifying loss” was the biggest challenge they faced;

- 68% reported feeling their maximum indemnity period is adequate;

- 39% indicated their existing BI policy provides either insufficient or no coverage for cyber risk, while 10% were unsure whether the policy covered cyber risk; and

- 35% have 12 months as the length of the maximum indemnity period (working group experts report 12 months is rarely an adequate timeframe).

Asked if risk managers believe the firm’s maximum indemnity period will be adequate in a worst-case scenario, the majority believed it would be.

In all, just 17% of surveyed risk mangers reported they were “extremely confident” that their BI values and limits are adequate. On the other end of the scale, 11% of respondents characterized themselves as having no confidence, with the middle ground (no confidence to extreme confidence) occupied by two groups (29% and 42%).

“Interestingly, when we break down this question to look at only the respondents who suffered a business income loss in the last five years, this group responded with only slightly more confidence than those who have not gone through a claim,” the report points out.

“This highlights just how under-prepared many organizations are to deal with a business income claim, even when they recently went through the process,” it notes. “The low rate of confidence in BI values indicates the need for organizations to do more analysis before BI limits and values are determined.”

Overall, 40% of respondents reported their company had experienced a BI loss and subsequent claim within the past five years, 58% had not and 2% were unsure.

“These results suggest that many companies and risk management professionals may not have not experienced a complex business interruption loss during their careers and, subsequently, BI claims may not be one of the top areas that concern the typical risk management professional,” notes the report.

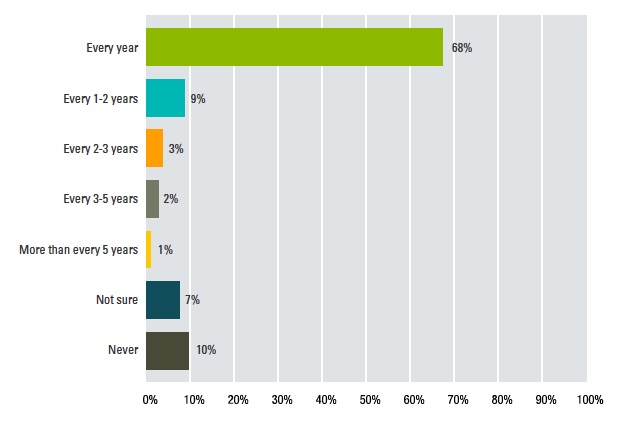

Asked how frequently BI insured values are reviewed against the company’s annual report and financial data, risk managers responded as follows:

Noting that it appears some risk managers still do not buy BI, “many that do buy it still rely on their insurers to analyze the risk and exposures,” the report states.

That said, “we are starting to see a trend of risk managers taking control of their own data, and getting back in the driver’s seat for negotiations with insurers,” it notes.

Less positive, just a third polled risk managers “provided estimated maximum exposure information. The overall exposure data for both property damage and business interruption is important in establishing the correct perception of risk,” the report adds.

“How do we know if the insurance we buy is competitive if we do not own the data and use it to compare insurers? How do we know if it is value for money if we haven’t quantified exposures?” the report asks.

“With their own data, surveys, BI exposure information and natural catastrophe modelling results, risk managers can compare the level of protection and value for money between insurers and establish for themselves the optimal position regarding cover, pricing, deductibles and limits,” it notes.

“The next step of loss scenario testing will be a vital ingredient in establishing a recipe for successful risk transfer,” the report adds.

Related: Business interruption due to breach top cyber risk concern for captive insurers: Aon

“With a world of emerging risks keeping business leaders up at night, risk professionals must prepare their organizations for the very real possibility that their business might suddenly come to a screeching halt,” RIMS CEO Mary Roth says in the statement.

“The exchange of knowledge and best practices makes it easier for risk professionals to ensure that appropriate measures are taken before, during and after an interruption occurs,” Roth continues.

“We have observed that risk managers that have suffered a loss in the last five years generally provide more information than those that have not,” states the report.

“Experience dictates that the clearer you are in relation to your exposures, and the more information you provide to your insurers, the smoother the claims process is likely to be,” it suggests.

More coverage of the RIMS 2017 Annual Conference & Exhibition

Silent cyber a big issue, most companies with insurance book have exposure: AIR Worldwide’s Stransky

Common language holds promise of advancing advance risk management efforts: Seaman

Risk professionals should move to fill the understanding gap around disruptive technologies

Damage to reputation/brand gets social, cyber jumps higher on risk list: Aon survey

Have your say: