A.M. Best reports spike in Canadian investment in U.S. insurance market

September 1, 2017 by Canadian Underwriter

Print this page Share

There is a “growing interest” among Canadian property and casualty insurers in the United States market, while on this side of the border, Aviva plc has became the Number 2 P&C insurer in Canada and the loss ratio in Canadian commercial P&C deteriorated 14.3 points in 2016, A.M. Best Company Inc. suggested in a report released Thursday.

“Anecdotal and statistical market data for the past 18 months indicates growing interest among Canadian P/C insurers in the U.S. market,” ratings firm A.M. Best said in its special report, Canadian Property/Casualty and Life Remain Stable as Economy Rebounds, While Housing Market Bears Watching.

“Anecdotal and statistical market data for the past 18 months indicates growing interest among Canadian P/C insurers in the U.S. market,” ratings firm A.M. Best said in its special report, Canadian Property/Casualty and Life Remain Stable as Economy Rebounds, While Housing Market Bears Watching.

Over the past 18 months, “Canadian investment in the U.S. market, either directly (i.e., by acquiring a U.S. operation or creating a new entity) or indirectly (i.e., by acquiring an international organization with significant operations in the U.S.), exceeded the level of investment in previous years,” Oldwick, N.J.-based A.M. Best said in its report on the Canadian industry. “Most notably, Intact’s announced acquisition of OneBeacon was driven by Intact’s explicit intent to expand into the U.S. market.”

Intact Financial Corp. announced May 2 it agreed to acquire Plymouth, Minn.-based OneBeacon for US$2.3 million. OneBeacon is traded on the New York Stock Exchange and majority owned by White Mountains Insurance Group Ltd., which announced May 2 it intends to “vote its shares” of OneBeacon in favour of Intact acquiring 100% of OneBeacon.

Another Canadian-based firm expanding into the U.S. is SCM Insurance Services Inc., which announced in 2016 it is opening a Chicago office and announced May 3, 2017 that it is acquiring St. Louis-based claims adjuster Nixon & Company Inc. SCM companies include, among others, data vendor Opta, engineering services provider Pario, investigations provider Xpera and independent adjusting firm ClaimsPro. SCM announced Aug. 31 it is receiving funding (without disclosing the amount or details) from private equity firm Warburg Pincus LLC. In 2014, SCM acquired the P&C business of Granite Global Solutions, which in turn owned Granite Claims Solutions, previously known as McLarens Canada and before that as Ponton Coleshill Edwards & Associates.

An acquisition of OneBeacon “will allow Intact to leverage the combined companies’ specialty lines experience while improving opportunities for additional scale in existing markets,” A.M. Best said in its report.

OneBeacon’s operations include International Marine Underwriters of New York City. In addition to ocean and inland marine, OneBeacon also writes general liability, auto, surety and professional liability.

In the Canadian P&C market, consolidation has “remained strong, with scale, diversification, and expertise among the recurring rationales for M&A,” A.M. Best said in its special report released Aug. 31.

In the Canadian P&C market, consolidation has “remained strong, with scale, diversification, and expertise among the recurring rationales for M&A,” A.M. Best said in its special report released Aug. 31.

Aviva Canada completed its acquisition of RBC General Insurance Company in 2016, leaving Toronto Dominion (TD) Bank as the only Big 6 bank that writes home and auto insurance. Aviva now has a deal with the Royal Bank of Canada Insurance in which Aviva Canada provides policy administration and claims services.

The RBC General Insurance acquisition “presented Aviva with an opportunity to achieve additional scale and market share in Canada” and “solidified Aviva’s spot” as the second-largest P&C insurer, when measured by direct premiums written, A. M. Best said.

The four Canadian P&C carriers with the greatest market share, in order, in 2016, were Intact, Aviva, Desjardins and TD, with $8.3 billion $5.1 billion, $4.5 billion and $3.0 billion in direct premiums written each, A.M. Best reported.

The Cooperators, Wawanesa and Lloyds each had $2.8 billion in direct premiums written last year in P&C while Economical and Travelers ranked ninth and 10th with $2.1 billion and $1.5 billion respectively.

The P&C industry in Canada had net premiums written of $41.1 billion last year, up 4.1% from $39.6 billion in 2015, A.M. Best reported, while the combined ratio deteriorated 2.7 points, from 95.5% in 2015 to 98.2% last year.

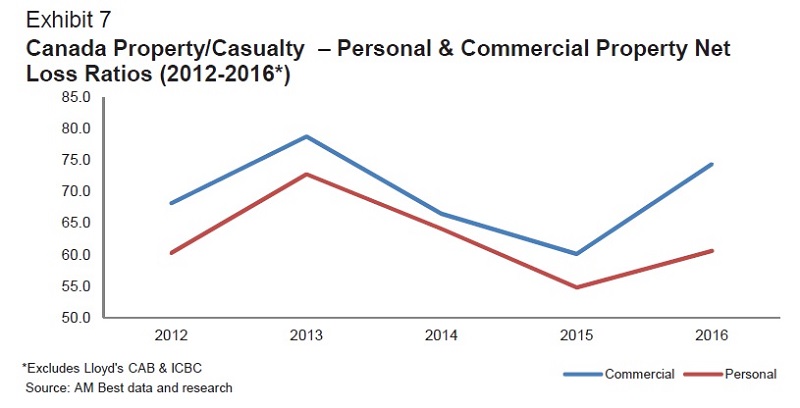

The loss ratio in personal lines increased from 54.8% in 2015 to 60.6% last year and in commercial lines the industry-wide loss ratio was up 14.3 points, from 60.1% in 2015 to 74.4% in 2016.

Have your say: