Markel Corporation reports consolidated net written premiums of US$3.162 billion for first nine months of the year

November 2, 2016 by Canadian Underwriter

Print this page Share

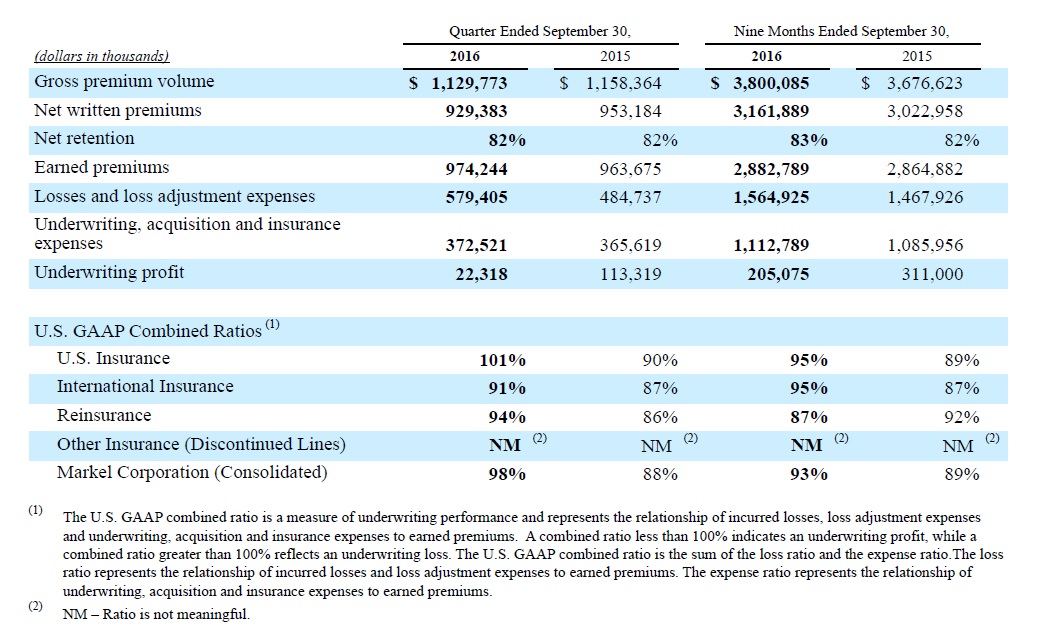

Glen Allen, Va.-based Markel Corporation reported on Tuesday consolidated net written premiums (NWP) for the nine months ending Sept. 30 of US$3.162 billion, up from US$3.023 billion in the same prior-year period.

Of the consolidated NWP for the nine-month period, US$1.694 billion was for U.S. Insurance (9M 2015: US$1.587 billion), US$681 million for International Insurance (9M 2015: US$700 million) and US$786 million for Reinsurance (9M 2015: US$736 million). For the three months ending Sept. 30, consolidated NWP totalled US$929 million, including US$562 million for U.S. Insurance (Q3 2015: US$536 million), US$210 million for International Insurance (Q3 2015: US$213 million) and US$157 million for Reinsurance (Q3 2015: US$204 million).

Of the consolidated NWP for the nine-month period, US$1.694 billion was for U.S. Insurance (9M 2015: US$1.587 billion), US$681 million for International Insurance (9M 2015: US$700 million) and US$786 million for Reinsurance (9M 2015: US$736 million). For the three months ending Sept. 30, consolidated NWP totalled US$929 million, including US$562 million for U.S. Insurance (Q3 2015: US$536 million), US$210 million for International Insurance (Q3 2015: US$213 million) and US$157 million for Reinsurance (Q3 2015: US$204 million).

“All three of our operating engines have made substantial contributions to our results in 2016,” said Alan I. Kirshner, executive chairman of Markel, in a press release. “While our underwriting results for the quarter were adversely impacted by unfavourable development on our medical malpractice and specified medical product lines, we continue to exercise underwriting discipline and our results for the nine months are in line with our expectations.”

According to its financial results, Markel’s combined ratio for the quarter was up 10 points to 98% from 88% in Q3 2015. For the first nine months of the year, the combined ratio was up four points to 93% from 89%. “The increase in the consolidated combined ratio for the nine months ended September 30, 2016 was driven by less favourable development on prior years’ loss reserves, partially offset by a lower current accident year loss ratio in 2016 compared to 2015,” Markel explained in its financial results.

The combined ratio for the quarter included US$50.1 million, or five points on the consolidated combined ratio, “of losses and loss adjustment expenses resulting from management actions during the third quarter in response to claim trends noted by our actuaries in our medical malpractice and specified medical product lines within the U.S. Insurance segment.” Of this amount, US$36.5 million represents reserve strengthening in prior accident years.

“The adverse development on both of these product lines was driven by an increase in the proportion of business written on classes with higher claim frequencies relative to other classes of business within these product lines over the last several years, including correctional facilities and contract physician staffing,” the financial results said. “Beginning in late 2015, we saw an increase in claim frequencies on these classes, which was inconsistent with the historical trends indicated by our actuarial analyses. In recent quarters, we have continued to see steady increases in claim frequencies, as well as increases in claims payments on these classes of business. As a result, we have given more credibility to this new trend, and management increased loss reserves accordingly.”

“The adverse development on both of these product lines was driven by an increase in the proportion of business written on classes with higher claim frequencies relative to other classes of business within these product lines over the last several years, including correctional facilities and contract physician staffing,” the financial results said. “Beginning in late 2015, we saw an increase in claim frequencies on these classes, which was inconsistent with the historical trends indicated by our actuarial analyses. In recent quarters, we have continued to see steady increases in claim frequencies, as well as increases in claims payments on these classes of business. As a result, we have given more credibility to this new trend, and management increased loss reserves accordingly.”

The combined ratio for the U.S. Insurance segment was 101% and 95%, respectively, for the quarter and nine months ending Sept. 30 compared to 90% and 89%, respectively, for the same periods of 2015. For both periods, “the increase in the combined ratio was driven by less favourable development of prior years’ loss reserves.”

For the International Insurance segment, the combined ratio was 91% and 95%, respectively, for the quarter and nine-month period compared to 87% for both periods. Markel attributed the increase in the quarter to “less favourable development of prior accident years’ loss reserves and a higher current accident year loss ratio, partially offset by a lower expense ratio compared to the same period of 2015.” For the nine months ending Sept. 30, “the increase in the combined ratio was driven by less favourable development on prior years’ loss reserves and a higher expense ratio, partially offset by a lower current accident year loss ratio compared to the same period of 2015,” the results said.

The combined ratio for the Reinsurance segment was 94% for Q3 2016 and 87% for 9M 2016 compared to 86% and 92%, respectively, for the same periods of 2015. Markel attributed the Q3 increase to “a higher expense ratio and less favourable development on prior years’ loss reserves compared to the same period of 2015.” For the nine-month period, the decrease in the combined ratio was driven by more favourable development on prior years’ loss reserves and a lower current accident year loss ratio, partially offset by a higher expense ratio compared to” 9M 2015.

Markel Corporation is a diverse financial holding company serving a variety of niche markets and underwriting specialty insurance products.

Have your say: