Personal lines cat ratio up 9.3 points at Intact due in part to Fort McMurray

February 8, 2017 by Canadian Underwriter

Print this page Share

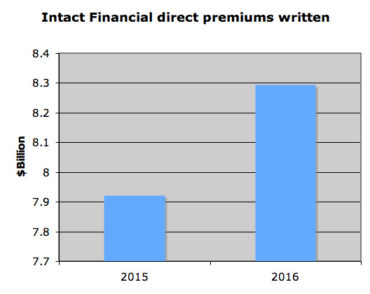

Intact Financial Corp. released Wednesday its financial results for 2016, reporting a 5% increase in direct premiums written and a 40% drop in underwriting income during a year when Canada’s most expensive natural disaster cost the firm $400 million before reinsurance.

For 2016, Intact’s combined ratio was 95.3%, up 3.6 points from 91.7% in 2015. Intact reported a combined ratio of 92.5% in the three months ending Dec. 31, 2016, up 3.9 points from 88.6% during the last quarter of 2015.

Direct premiums written were up 5% from $7.922 billion in 2015 to $8.293 billion in 2016. Direct premiums written were $2.0043 billion in the latest quarter, up 5$% from $1.948 billion in Q4 2015.

Intact Financial’s “significant operating subsidiaries” are Intact Insurance Company, Belair Insurance Company Inc., The Nordic Insurance Company of Canada, Novex Insurance Company, Jevco Insurance Company, Canadian Direct Insurance Inc., Trafalgar Insurance Company of Canada, Equisure Financial Network Inc., Canada Brokerlink Inc., Intact Farm Insurance Inc. and IB Reinsurance Inc.

Company-wide, broken down by line, direct premiums written for 2016 were $3.792 billion in personal auto, $2.03 billion in personal property, $1.768 billion in commercial property & casualty and $703 million in commercial auto.

Underwriting income dropped 40%, from $628 million in 2015 to $375 million in 2016.

The wildfire last May that resulted in the evacuation of Fort McMurray, Alta had a $175-million impact, net of reinsurance, on Intact’s financial results for 2016, the company said in its management discussion and analysis. The cost before reinsurance was about $400 million, Intact said of the Fort McMurray wildfire, which to date is Canada’s costliest natural catastrophe when measured by insured losses. The impact after tax on Intact was $128 million.

Underwriting income for Q4 dropped 31%, from $221 million in 2015 to $153 million last year.

In personal auto, Intact reported a current-year loss ratio of 78.5% in 2016, up 4.6 points from 73.9% in 2015, “due to higher weather-related claims frequency and industry pool losses,” Intact said.

The industry pools consist of the Facility Association as well as risk sharing pools in Alberta, Ontario, Quebec, New Brunswick and Nova Scotia.

“Industry pools were impacted by deteriorated trends across the country, affecting both current year and prior year results,” Intact said in its MD&A.

“The impact of assumed industry pools on personal auto underwriting income was a loss of $24 million in Q4 2016, compared to a loss of $6 million in Q4 2015,” the company stated. “On a full year basis, the impact was a loss of $48 million in 2016, compared to a loss of $6 million in 2015. The deterioration was mainly explained by unfavourable trends in Ontario, claims cost inflation across the country and an overall increase in claims frequency.”

The combined ratio in personal lines deteriorated five points, from 85.9% in 2015 to 90.9% in 2016. The cat ratio was 11.6%, up 9.3 points from 2.3% in 2015, driven by “industry record-breaking cat losses, including the Fort McMurray wildfire and severe storms across Canada.”

In commercial p&c, Intact reported a combined ratio of 90.2% in 2016, up 3.4 points from 86.8% in 2015. The commercial auto combined ratio improved 4.4 points, from 99% in 2015 to 94.6% last year.

Net income attributable to shareholders was $541 million in 2016, down 23.4% from $706 million in 2015, Intact reported. Net income attributable to shareholders was $171 million in the most recent quarter, down 27% from $198 million in 2015.

Have your say: