Trusted advisors take centre stage

July 1, 2020 by David Gambrill, Editor in Chief

Print this page Share

About one month into the novel coronavirus pandemic, Joseph Carnevale, president of the Insurance Brokers Association of Ontario (IBAO), made a spirited declaration about the value of an insurance broker.

“I think for the longest time, as brokers, we have always promised our clients that we would be there in their time of need,” Carnevale said as a panellist on a Canadian Underwriter webinar about business continuity. “We not only have a great relationship with them, we not only understand their needs and provide them with the right products and the right service to support that, but we would be there for them in their time of need…

“This particular pandemic has provided us the opportunity to actually live that and to demonstrate that. We are the trusted advisor. More so than words, we are living it, we are breathing it, we’re doing it, and we are acting on that.”

What is a trusted insurance advisor?

The Insurance Brokers Association of Canada (IBAC), Canada’s national broker association, lays out three pillars of what the industry commonly refers to as the “broker value proposition.” Basically, brokers provide advice, choice and advocacy for the insurance consumer.

Brokers work for consumers, not insurance companies. Because of this independence from the manufacturers of the product (the insurance policy), brokers are able to:

- Offer consumers a wide variety of products and price comparisons from a number of insurance companies

- Advise on a customer’s specific risks and suitable insurance protection

- Provide clear information and explain policy details

- Support and represent customers if they need to make a claim

Consumers are of course the best judge of whether brokers are practicing what they preach. And so, Canadian Underwriter canvassed the opinions of 653 Canadians who purchased home and auto insurance from a broker, as well as representatives of 159 Canadian businesses (most of them small businesses), and asked them what they thought about the service they were getting from their brokers.

We based the survey questions on the very services that brokers say they provide to consumers. We conducted the survey Mar. 6 to 13, just before the pandemic went into full effect (the World Health Organization declared the novel coronavirus to be a global pandemic on Mar. 11). At that time, brokers were helping consumers navigate through a different form of crisis: A hardening market cycle in the industry meant that consumers’ insurance premiums were increasing while their coverage options were shrinking.

Read the second part of our four-part series – Looking in the Mirror

Read the third part of our four-part series – We need to talk…

It was not an easy time to be a broker, as consumers had every reason to be frustrated about rising insurance costs. And yet, our 2020 Trusted Advisor Survey suggests that if they were upset, it wasn’t about the service they were getting from their brokers.

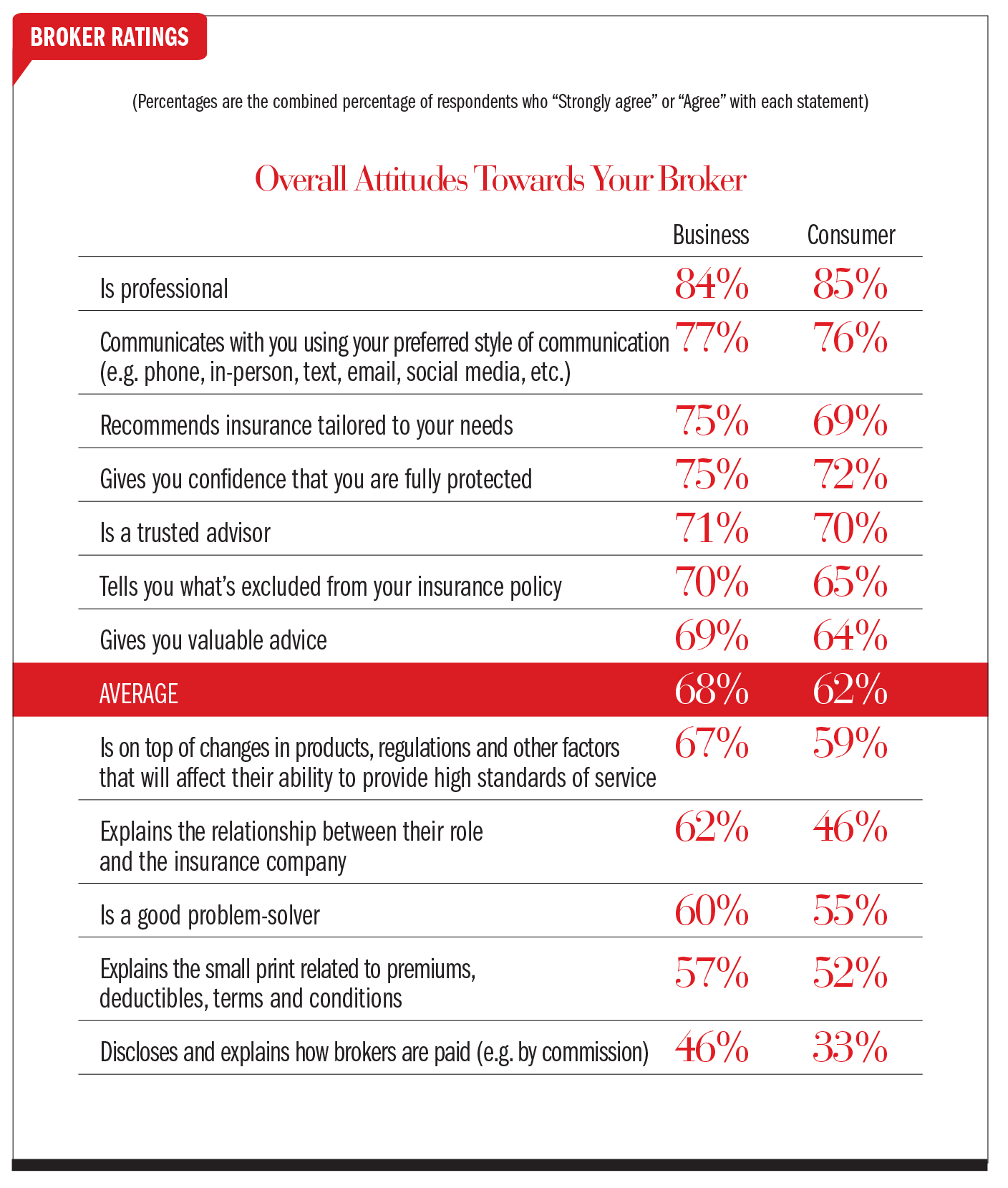

On the contrary, the survey results indicate that brokers were already living up to their “trusted advisor” status pre-COVID, during the dreaded hard market. Seventy-one percent of business customers and 70% of home and auto insurance customers surveyed either strongly agreed or agreed with the statement that their broker is “a trusted advisor.”

What is a trusted advisor?

Our survey asked consumers to agree or disagree with a series of 12 statements that define the broker value proposition. Overall, the baseline level of satisfaction for business insurance consumers — the percentage of those who either strongly agreed or agreed with the statements — was 68%. For home and auto insurance consumers, the consumers’ baseline satisfaction score was 62%.

When you look at the scores above those baseline averages, the survey showed high overall satisfaction with brokers in several key areas. For example, almost 80% of home, auto and business insurance consumers agreed that brokers were professional. They also agreed that brokers:

- Communicated using the consumer’s preferred style of communication

- Recommended insurance tailored to their needs

- Made consumers confident that they were fully protected

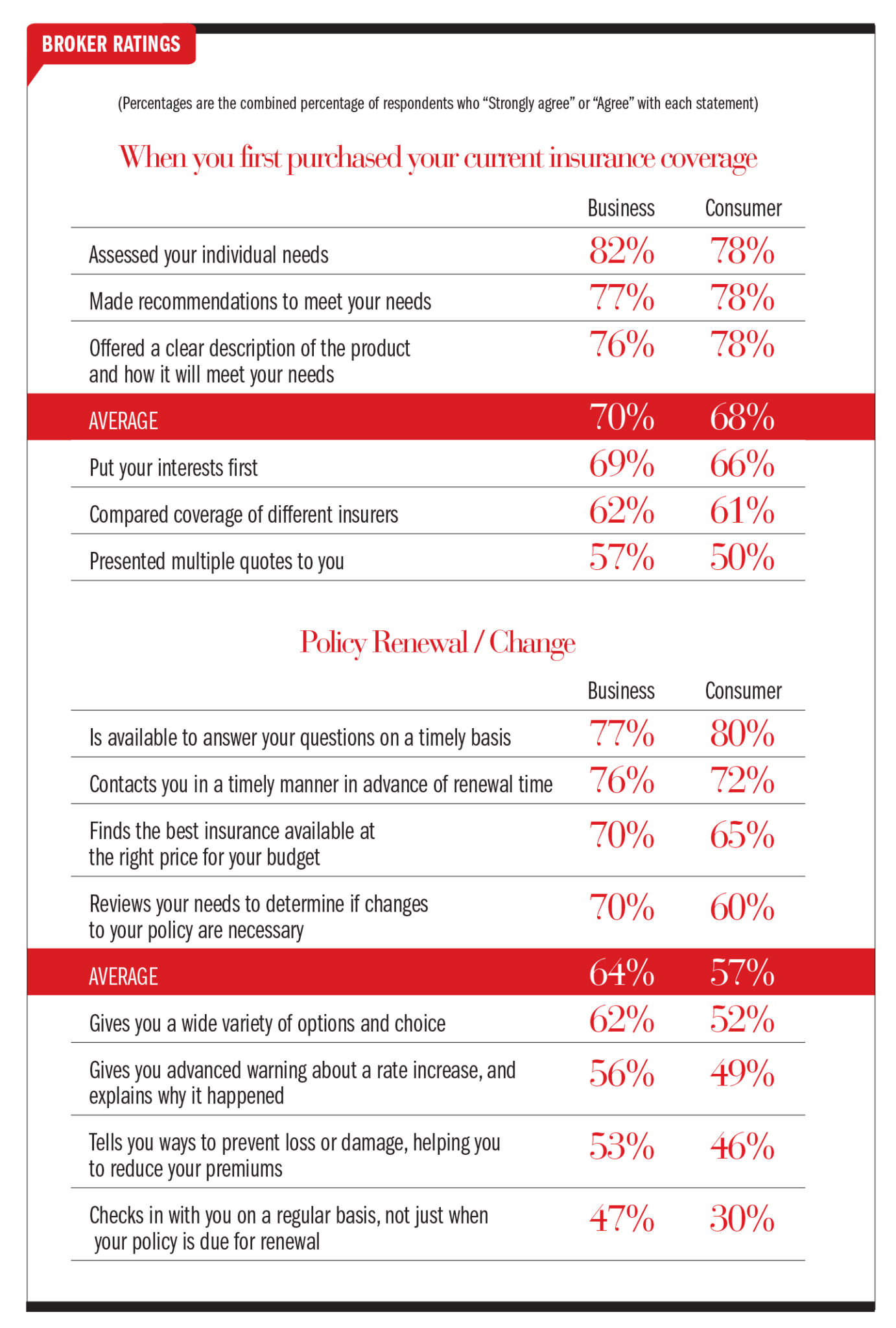

Elsewhere, customers were asked about the service they received from brokers during the new business and policy renewal/change phases of the insurance purchase process. When consumers first purchased their insurance, brokers scored well above average on assessing individual needs, making recommendations that meet those needs, and offering a clear description of the product.

“A lot of these statistics are positive,” Colin Simpson, CEO of the IBAO, said of the survey results in an interview. “Take, for example, the assessing of personal needs, and making recommendations that meet their needs, and offering a clear description of the product. I mean, what else do you need professional advice for? This is all totally bang-on. It’s totally what brokers are there for. It’s what they do. They are doing their jobs and they are doing their jobs well.”

As for when brokers were doing policy renewals and changes, brokers in both commercial and personal lines scored well on availability to answer questions, contacting clients in a timely manner in advance of renewal, and finding the best insurance available at the right price for a consumer’s budget.

“Where the survey talked about policy renewal and policy changes, I was pleased to see that customers feel there is transparency in what is being delivered,” said Roger Hacala, past president of the Toronto Insurance Council (TIC), a national commercial brokarage association, and national practice leader of professional and financial services for BFL Canada Risk and Insurance Services. “This would be around the right price for budgets, reviewing customers’ policies, and making policy changes where required — that type of thing. Those are all the proactive things that the broker is doing, which is great.”

Consumer Expectations

The survey revealed three main opportunities for brokers to get to know their clients better. For example, consumers appear to want to hear more from their brokers about:

- Comparing and providing multiple quote options

- Advance warning of rate increases

- Advice for mitigating risk and preventing losses

In some of these areas, it may be that brokers need to explore alternative ways to provide more information or context to their clients, says Brenda Rose, vice president of FCA Insurance Brokers.

“Overall, when I look at this survey from a very high level, I see there isn’t always a full alignment of expectations here,” says Rose. “If a customer is rating their broker below average on any of these points, then we haven’t met their expectations. Perhaps we might think that the expectation isn’t possible. But if that’s the case, then we need to help the customer understand that.”

The opportunities for improved communication came up at various stages of the insurance purchasing process.

FIRST INSURANCE PURCHASE

Comparing and providing multiple quote options

When first purchasing insurance, customers scored brokers “below average” on comparing the coverage of different insurers and presenting multiple quotes to the consumer. (Keep in mind the baseline average agreement for each of the statements in this section was quite high — 70% for consumer clients and 68% for personal lines customers.)

Providing choice is a key pillar of the broker model. While most brokers are in fact pursuing quotes from multiple markets and assessing them behind the scenes, that may not necessarily be obvious to the insurance purchaser.

“For brokers, I would say sometimes it’s like the duck on the water,” said David Pettigrew, president and CEO of Harvard Western Insurance. “You don’t see the feet underneath the water going crazy. You just see the duck gliding on the surface. Sometimes the client may not see all of that activity happening behind the scenes.

“The challenge we have as brokers is that we do a lot of work that we don’t tell the client. These results are a good reminder that if you don’t share with clients what you’ve done, they might not understand that it happened. A good example would be: How many options did you look at? How did they all compare? Brokers have quite likely done that work on behalf of the client, but they don’t always share this information. So, it’s always a good reminder to say, ‘The client doesn’t necessarily know what you’ve done until you tell them.’”

That said, there is a balance to be struck when it comes to presenting options and multiple quotes to consumers, brokers say. Vicki Livingstone, manager at Freeman Insurance Agencies Ltd. in Innisfail, Alta., notes that some brokers will lead with their best recommendation, and then provide one or two other options for comparison’s sake. Commercial lines brokers are more likely than personal lines brokers to provide a formal, line-by-line comparison, Hacala says. In part, that’s because commercial insurance products tend to be more specialized (and less commoditized) than in personal lines. Also, several brokers observed that they were conscious of their clients’ time when providing options.

Simpson said that in some circumstances, presenting the full spectrum of options to a consumer may wind up doing more harm than good.

“When a broker services a consumer, they have to spend time with that consumer to understand their risk profile,” he said. “Based on that individual’s risk file, and based upon that broker’s experience in the industry, quite often there will be a clear communication path to go down. So to offer products, services or prices that do not address that individual’s requirements could be seen as either: a) good, open communication, or b) very confusing, and end up with the client choosing something that is not appropriate. So, it’s the broker’s job to make sure they provide advice to the client that best matches their needs. That can be done all sorts of different ways, depending on the client.”

POLICY RENEWAL/CHANGES

Advance warning on rate increases

Customers are clearly looking for brokers to give them a heads-up about upcoming rate increases.

The trouble is, as brokers point out, brokers are not in control of market pricing. Often, they will find out about the impact of specific rate increases at the same time as their customers.

“You don’t actually know,” Simpson said of the beginning of the industry’s hard market cycles. “That is the problem. Until you do a quote or a renewal, you don’t know for each customer [what the rate increase will be].

“For example, say an insurer says, ‘We’ve filed for a 4% rate increase.’ It doesn’t mean every client gets 4%. Some could be 15%, some could be minus-five. You don’t know until you pull the individual risk and get a new rate. So it’s very difficult for any broker to focus on a narrow risk and explain what is going to happen to that risk from a rate point of view. I know it’s frustrating from a consumer’s perspective as to why the industry can’t be more predictable. But if it was, we wouldn’t be employing hundreds of actuaries.”

Consumers may not be aware of what brokers are doing in the trenches on behalf of their clients, some brokers say. And so what seems like a victory for a broker on behalf of the client may in fact be viewed differently by the client.

Hacala provides the following example. In some lines, he says, commercial brokers “anticipated a 15% increase and [the client] ended up getting a 25% increase. We beat down the markets from a 35% increase down to that 25% increase. But I think that doesn’t translate well, as far as how that comes through [to the consumer].”

Hacala said the matter may come down to how the broker manages delivering bad news to the consumer. In the hypothetical scenario above, for example, suppose the broker first tells the client to expect a 15% rate increase. Then the broker finds out from the carrier that it will be a 35% increase. The broker then negotiates the rate down to a 25% increase. One way to message that to the client, as Hacala says, is to make sure the client knows the full context.

For example, suppose the broker did the actual comparison for the client: “It was coming in at this, but we went back, we negotiated, and we got it down to this. I realize this is above your budget expectation, but it’s also better than industry targets.” Perhaps this a better way to message the bad news, Hacala suggested, although nothing is foolproof. “It is a tough thing, because the broker may have done a good job, but they may have fallen short in the client’s eyes because they said, ‘Well, you told me this.’”

More broadly, says IBAC president Kent Rowe, “giving advance warning about rate increases and explaining why they happen, I think that’s an opportunity for us to improve. We’ve been mired in a hard market, we’ve been there for a while, and we probably will stay there. I think it’s a lesson for us to have those discussions with our clients and we keep them informed and protected.”

In some ways, the hard market presents a good opportunity for brokers to connect more deeply with their customers, Rowe added.

“In the hard market, when we are operating in a challenging environment, it does provide more reason for brokers to contact their clients,” Rowe said. “That’s just the nature of the business. When you have capacity or pricing problems, we want to make sure we are trying to overcommunicate in those instances, and making sure that we are managing client expectations. These are tricky circumstances.”

Looking for risk advice

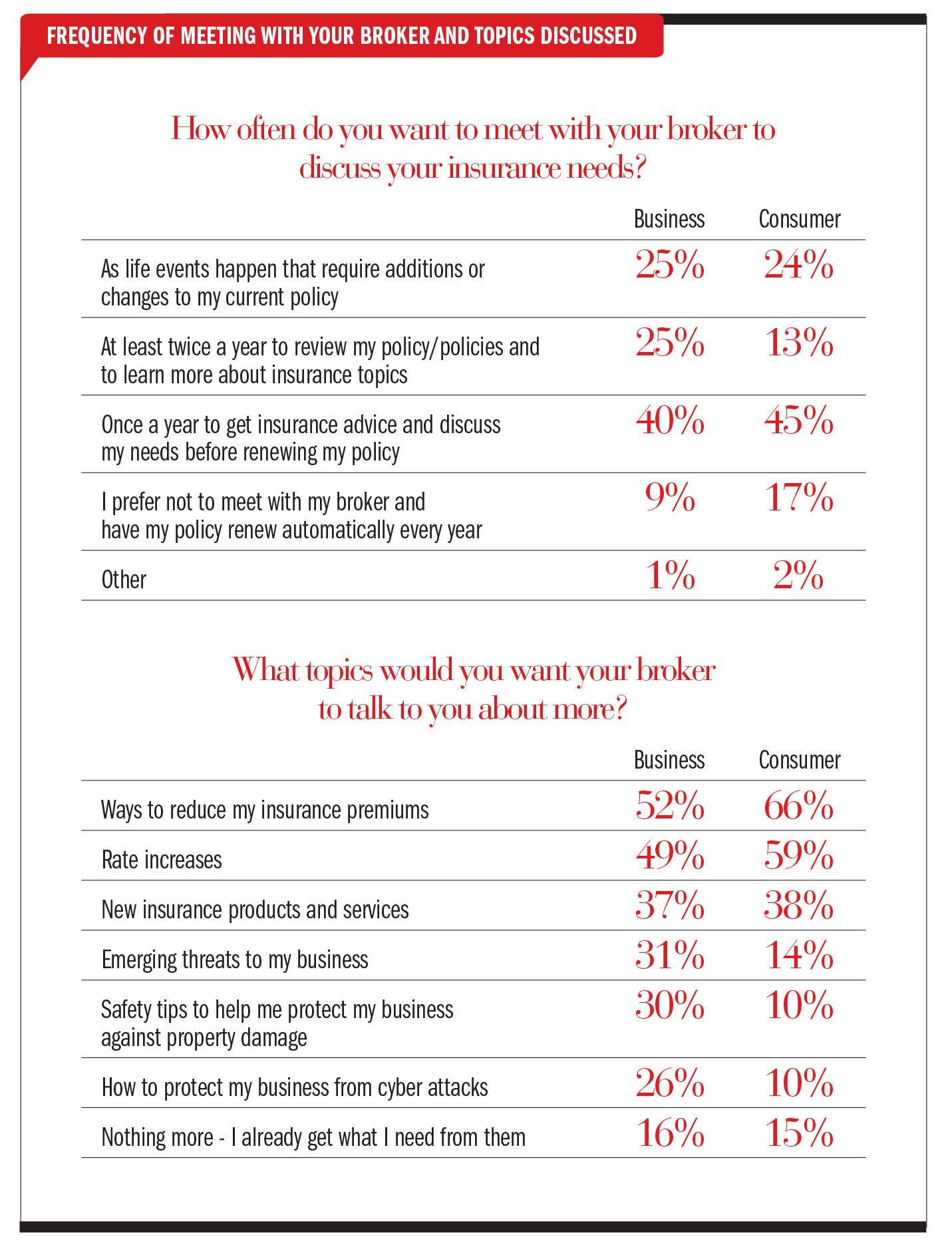

Customers are looking to their brokers for more information about how to reduce their losses. In the policy renewal portion of the survey, customers rated their brokers below average on telling them ways to prevent loss or damage.

Elsewhere in the survey, consumers were asked, “What topics would you want your broker to talk to about more?” The top answer for both commercial lines clients (52%) and personal lines customers (66%) was: “Ways to reduce my insurance premiums.” On the commercial side, 31% of business clients surveyed said they wanted to talk to their brokers more often about “emerging threats to my business.” Another 30% wanted to hear more about “safety tips to help me protect my business against property damage.”

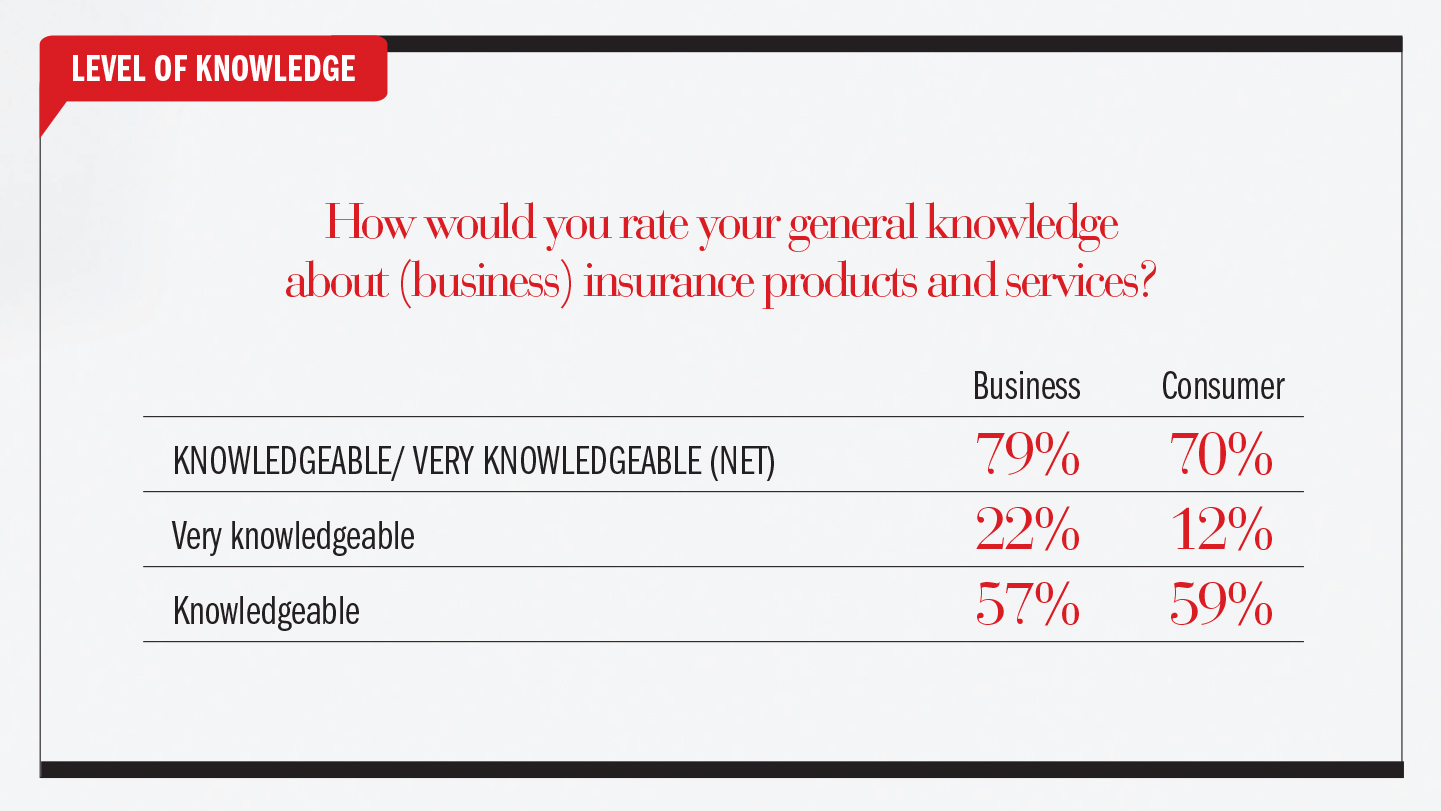

On the commercial side in particular, clients expect to hear more from their brokers about risk-based advice that doesn’t simply reflect a transactional price quote and coverage explanation. It’s a shifting expectation of business clients who have more access than ever before to information about their insurance products and services. Seventy-nine percent of consumers in our Trusted Advisor Survey rated themselves as either “very knowledgeable” or “knowledgeable” about business insurance products and services. Summed up simply, the new attitude for commercial clients may be, “Tell me something I don’t already know.”

A trusted advisor is part of the client’s decision-making process, and is not just an order-taker, as Rowe puts it. “One of the bigger positives that I took out of this survey is that I think clients view us more as being a trusted advisor, versus somebody through whom they transact business,” he said. “A trusted advisor is someone you call before you make a decision. Somebody you transact business with is someone you call after you have made the decision.”

Rowe and Pettigrew believe brokers are adapting to these evolving consumer expectations.

“All of the leading brokers, I would say, are moving towards a risk advisor skill set and thought process,” said Pettigrew. “They are helping educate clients on understanding their risks and navigating them, and then using insurance where necessary or desirable; not just providing insurance-specific risk services. This is a trend, especially in the commercial insurance market.”

Access to information about claims trends and loss data is key to succeeding in this new role. As Pettigrew points out, brokers will need to improve connectivity to insurers’ back-end systems to access the kind of claims and loss trends information that would be beneficial for clients to know.

But there may be a limit on how far a broker might stray into the territory of risk guidance. “Providing other insurance options to address the risk — that it’s not just about a price, and it’s not always just about buying more insurance — that’s one conversation,” as Rose points out. “But the whole concept of risk control in a physical sense is an entirely different qualification. And not everyone who has just graduated and got a [broker] licence is equipped to do that. It also depends on the nature of the risk that you are talking about.”

Rowe is confident brokers will adapt to customers’ expectations as they evolve. “Brokers are talking every day about enhancing customer experience,” he says. “A huge part of that is learning what your customer wants, and delivering on those wants. For the most part, I think brokers are doing a tremendous job in that area. As brokers, we have been very good in the past at adapting to various market conditions. We will continue to evolve and match the needs of our customers with the services that we offer.”

Consumers would seem to agree, the survey results show.

“I’m really happy to see that [the survey shows] we are able to give clear descriptions on the product, we are assessing their needs, and we’re making recommendations that suit their needs,” Livingstone said. “We are trusted advisors. I think that’s awesome. That is the definition of a broker.”

Have your say: