Canadian M&A ahead of last year as private equity, outbound deal activity increases through Q3: PwC Canada

November 8, 2017 by Jason Contant, Online Editor

Print this page Share

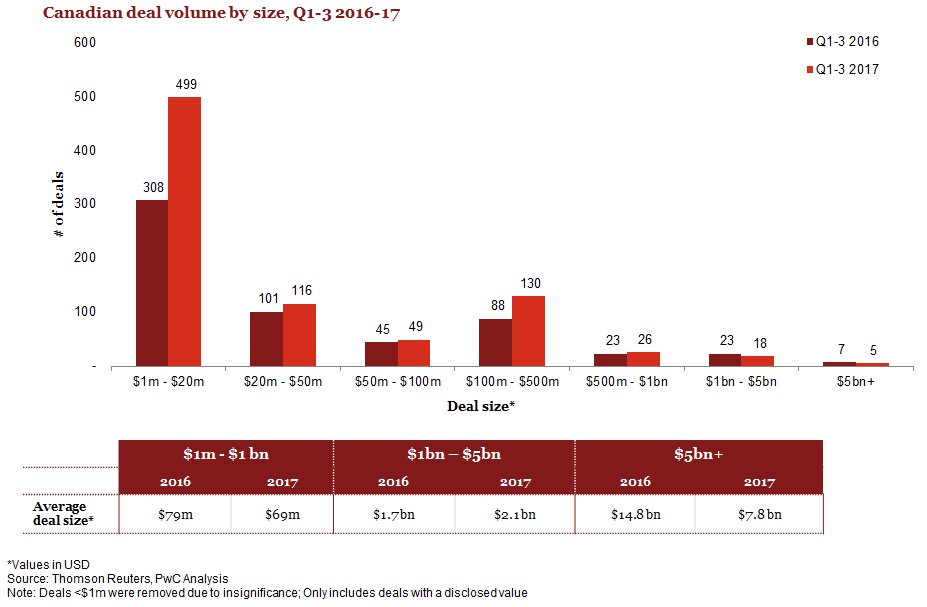

The number of Canadian mergers and acquisitions (M&A) through the third quarter of this year increased to 1,879 from 1,522 during the same period in 2016, according to PwC Canada’s first Deals report, released on Monday.

A PwC Canada spokesperson told Canadian Underwriter that the 23% increase from 1,522 deals to 1,879 deals includes deals involving companies with headquarters in Canada as either the buyer or seller. This includes domestic deals (Canadian buyer and seller), inbound deals (Canadian company being acquired) and outbound deals (Canadian company doing the acquiring). Deals less than US$1 million are excluded and many companies do not disclose a deal value.

A PwC Canada spokesperson told Canadian Underwriter that the 23% increase from 1,522 deals to 1,879 deals includes deals involving companies with headquarters in Canada as either the buyer or seller. This includes domestic deals (Canadian buyer and seller), inbound deals (Canadian company being acquired) and outbound deals (Canadian company doing the acquiring). Deals less than US$1 million are excluded and many companies do not disclose a deal value.

In insurance “including life/health, property/casualty, brokers and reinsurance,” there were 29 deals in the first three quarters, the spokesperson said, adding that there were only four deals in the consumer financial services subsector.

United States remained the largest outbound destination, according to the Deals report, with deal volume growing 27% during the period (from 245 to 310).

The overall Canadian M&A market deal volume is up 23% compared to Q1-Q3 of 2016, but deal value has taken a modest dip, PwC Canada reported in a press release. There were fewer ‘mega-deals’ (over US$1 billion) so far in 2017, which impacts the overall average deal values. Outbound deals reflected the overall market, as volume increased 17%, but at a lower average deal value, the release noted. “Large deals of US$1B+ have seen a slight decline in volume,” wrote David Planques, a partner and national deals leader with PwC Canada. “However, it’s important to note that these megadeals are somewhat anomalous: they don’t really drive the market, but when they happen (or don’t happen), they can distort overall market data.”

Outbound deals to the U.S. were strong, with volume growing largely due to deals in the technology and real estate sectors. In tech, there was strong growth in IT services and consulting deals, while software deals were roughly flat. As for the real estate sector, development and operations businesses saw strong deal activity, while real estate services were flat. Consistent with the broader trend, smaller outbound deals to the U.S. between (US$50 million – US$1 billion) saw robust growth, while outbound mega-deals to the US (>US$1 billion) were down slightly.

“The boost in deal volume in 2017 makes for interesting analysis,” Planques suggested in the release. “The strong North American economy and large pools of capital to invest contribute to a very active deal market in Canada despite the high valuations and an 80 cent Canadian dollar (on average). Buyers should be focused on ensuring they have a strong value creation strategy for acquisitions.”

“The boost in deal volume in 2017 makes for interesting analysis,” Planques suggested in the release. “The strong North American economy and large pools of capital to invest contribute to a very active deal market in Canada despite the high valuations and an 80 cent Canadian dollar (on average). Buyers should be focused on ensuring they have a strong value creation strategy for acquisitions.”

Through Q3, private equity (PE) firms and pension funds have been highly active in the M&A space, with activity growing almost 40% in volume of buy-side and sell-side deals. The average deal size has increased by approximately 20% in 2017 for those deals with disclosed value.

“The M&A market is hot at the moment,” Planques wrote in the report. “Throughout the past several quarters, there’s been a steady uptick in volume of private equity (PE) and pension fund buy-side and sell-side deals. This is evidence of a highly competitive market with aggressive bidding, steadily rising multiples, and a lot of capital that needs to be deployed. High deal volume and high prices will drop at some point, most likely when sentiment shifts in the broader public equity market,” Planques suggested. “However, it’s unclear when that correction will happen and whether it will impact all sectors or only certain industries.”

PwC reports that four key takeaways have important implications for active buyers and sellers in the M&A space:

- Now may be a good time to sell – For business owners considering selling, now might be the right time. Valuations are high and there is plenty of capital looking for deals, including a very well-funded sector with “plenty of dry powder. While multiples may still continue to rise, the market is in your favour if you’re considering an exit now”;

- Buyers should “stress test” purchases – If there is capital to deploy, a strong investment rationale is needed to justify the high valuations that may be needed to pay to land a deal. “More and more, we’re seeing sophisticated players use data and analytics in their stress testing to consider these factors and others to determine how their business will respond if there’s a downturn,” the report said;

- Post-deal value creation is key – Buyers need to have a concrete plan for changing the way the business operates, rather than just buying and holding. A number of fund are leading the way on using technology and analytics to drive increase value from their investments;

- Go where the market is less crowded – In the US$25–$50 million “bucket,” multiples are lower and there’s generally less competition (including less PE focus). For example, instead of buying a single business for US$100 million, look for smaller businesses where there are consolidation opportunities through bolt-on acquisitions (albeit that multiple deals may increase execution risk).

Have your say: