A.M. Best projects combined ratio of 100.3% for U.S. industry in 2017

January 30, 2017 by Canadian Underwriter

Print this page Share

The industry-wide combined ratio of the United States property & casualty insurance industry is estimated to have deteriorated by 2.4 points to 100.7% in 2016, A.M. Best Company Inc. said in a recent report.

The decline in underwriting performance “was driven” by “a return of catastrophe losses to a more historically average level and a reduced benefit of favorable development of loss reserves,” stated Oldwick, N.J.-based A.M. Best in the report, titled Profitability Slides, Surplus Growth Slows and Competition Intensifies for U.S. Property/Casualty Insurers.

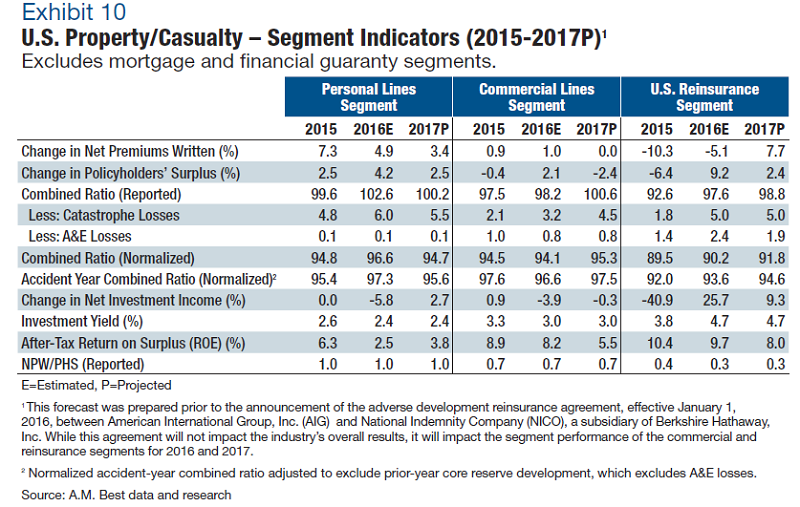

A.M. best is projecting a combined ratio for U.S. P&C of 100.3% in 2017.

A.M. best is projecting a combined ratio for U.S. P&C of 100.3% in 2017.

The combined ratio was 106.5% and 102.5% in 2011 and 2012 respectively, while the industry made an underwriting profit in each of 2013, 2014 and 2015.

A.M. Best estimates industry-wide net premiums written were $533.5 billion in 2016 and is projecting that figure to rise to $546.7 billion in 2017. All figures are in United States dollars.

Net premiums written were $519.5 billion in 2015, of which $288.5 billion was in personal lines, $189.9 billion was in commercial lines and $41.1 billion was in reinsurance.

A.M. Best is estimating net premiums written in 2016 at $302.7 billion in personal lines, $191.8 billion in commercial lines and $39 billion in reinsurance.

The company is estimating a combined ratio of 102.6% in commercial lines for 2016 and projecting a 2.4 improvement to 100.2% this year.

In personal lines auto, A.M. best is anticipating a combined ratio for 2016 of 108%.

“Loss cost trends have seen pressure mounting from the rising inflation of medical and auto repair costs,” A.M. Best said in the report. “As new car technologies continue to become more sophisticated and vehicle values rise, repairs are becoming more costly and more damaged vehicles are being taken as total losses.”

The ratings firm suggested that U.S. auto insurers “have continued their investments to develop and improve tools used in data analytics and usage-based insurance.”

“The further penetration of usage-based insurance has increased in recent years, and more advanced pricing segmentation has been achieved as insurers can now better understand the unique driving characteristics of each insured.”

A.M. Best estimates the combined ratio in home insurance deteriorated by 5 points to 97% in 2016, “reflecting some accumulating losses from weather activity that is less than catastrophic, and indicative that rates may not be quite adequate yet.”

The report noted that in 2016, Hurricane Matthew made landfall in the Florida panhandle.

“While actual losses from Matthew were well under initial estimates, they were nonetheless considerable,” A.M. Best added. “In addition, the homeowners line also faced a similarly volatile tornado, hail, and thunderstorm season as has become customary in recent years.”

There were also numerous wildfires in the U.S. southeast, “including the fire that caused significant damage in Gaitlinburg, Tennessee.”

In commercial lines, A.M. Best is projecting a combined ratio of 100.6% this year and estimating a combined ratio of 98.2% in 2016.

“The expected deterioration in the 2017 calendar-year underwriting results is driven primarily by an increased estimate of catastrophe losses in 2017 to a more normalized level and declines in pricing for the majority of commercial lines,” A.M. Best stated in the report, adding that catastrophe losses in commercial lines were $6 billion in 2016.

“In 2016, commercial lines writers recorded favorable core reserve development equating to 1.6 points on the segment’s combined ratio, compared with 3.1 points in 2015,” A.M. Best reported. The favorable development in 2015 was “net of an unusual level of reserve actions taken” by American International Group Inc. during the fourth quarter of that year, A.M. Best added.

In its annual report released in early 2016, for calendar year 2015, AIG reported $3.386 billion in prior year development in commercial P&C in the United States and Canada. Of that, $1.529 billion was in excess casualty.

On Jan. 20, 2017, AIG said in a release it “expects a material prior year adverse development charge” during the fourth quarter of 2016. AIG is scheduled to release its 2016 financials Feb. 14.

That announcement “highlights the challenges that AIG management continues to face in reserving, pricing, and handling this longer tail commercial lines business, and the effectiveness of the group’s enterprise risk management function,” A.M. Best said in a separate release Jan. 26.

Have your say: