The Power of Broker Specialization

October 27, 2018 by David Gambrill

Print this page Share

This story is one in a series reporting on the results of 2018 National Broker Survey, conducted by Canadian Underwriter. The survey of more than 800 P&C brokers nationally was designed to identify the success strategies of both producers and principals. Find other instalments in the series here and our overview package in our October 2018 issue.

The Power of Broker Specialization

In the 1994 spy movie The Specialist, two CIA explosives experts played by Sylvester Stallone and James Woods are on a mission to blow up a car transporting a South American drug dealer. But when Captain Ray Quick, played by Stallone, sees a young girl in the car, he calls to abort the mission. Colonel Ned Trent, played by Woods, is having none of it, and the mission proceeds, killing the target and the young girl. Traumatized by the incident, Stallone’s character quits the CIA and starts his own business as a freelance hit man who specializes in “shaping” his explosions so that they don’t kill innocent people.

Welcome to the new era of market segmentation.

Brokers are responding to the new era by taking an increased interest in specialization, as evident in the National Broker Survey.

[click to enlarge]

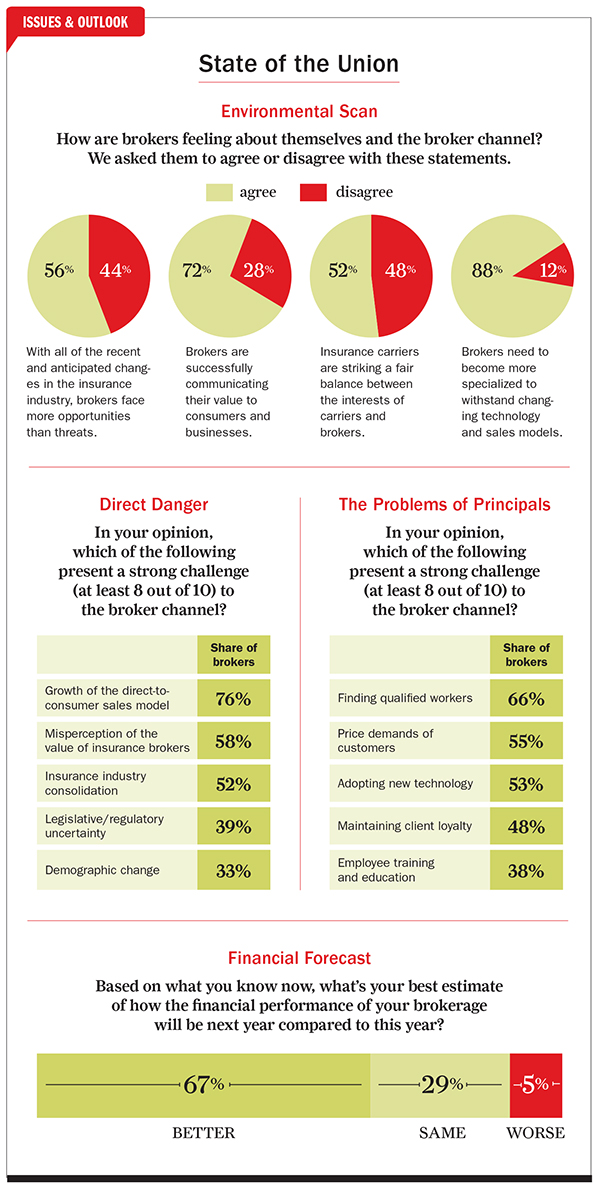

One survey asked brokers how they felt about general, high-level statements related to their business [see State of the Union infographic, left]. The highest level of agreement (88%) was expressed for the following statement: “Brokers need to become more specialized to withstand changing technology and sales models.”

One survey asked brokers how they felt about general, high-level statements related to their business [see State of the Union infographic, left]. The highest level of agreement (88%) was expressed for the following statement: “Brokers need to become more specialized to withstand changing technology and sales models.”

Of those who agreed, more than half did so strongly. The level of agreement was roughly the same for personal lines brokers (89%) as it was for commercial lines brokers (between 90 and 95%, depending on the concentration of commercial business).

“Historically, there was a hesitancy to stake your claim on a single area because you never wanted to exclude yourself from other opportunities,” says Michael Loeters, past president of the Toronto Insurance Council (TIC), which promotes the common interests of large commercially-focused insurance brokers with an office in the Greater Toronto Area. “But, as the market has become more sophisticated, clients expect a broker to walk into their office with an understanding of their unique risks to be able to architect an insurance program. Specializing is the way to do that.”

So, what does specialization mean, and how do they do brokers do it?

“The best way to describe specialization is to say that it creates deep-seated bench strength in a given industry,” says Tina Osen, president of Hub International Canada. “This is not just the broker handling the coverage placement, but also risk services and claims capabilities. It’s a holistic offering to the client in their given industry around any insurance-buying needs they might have.”

Specialization encompasses everything from pre-loss mitigation service to post-loss claims response. Examples of specialized risk mitigation services include identifying a specific industry’s loss exposure trends, and designing special packages to mitigate those risks. Interviews with brokers across the country suggest four main ways to specialize:

• Offer specialized knowledge and advice to clients.

• Provide unique insurance products, programs and/or services based on individual producers’ particular aptitudes and enthusiasms.

• Narrow the focus of the entire brokerage to specific lines of business.

• Providing service in traditional insurance lines using a unique distribution method such as purely digital platform.

A brief summary of these types of services is offered below:

Specialized knowledge

When brokers offer specialized advice to clients, this is often done to differentiate brokers from their competitors (for example, by giving advice, brokers provide value not offered by other brokerages, insurance companies or disruptors). But today brokers need to keep ahead of the advanced general knowledge of their consumers, who can learn a great deal by conducting a basic Google search. In essence, brokers need to justify their value as a ‘middleman’ in the insurance purchase.

“Where we lend value is helping clients understand what’s important in their particular given area, and what’s critical to them,” Osen says. “Where do we see the risks in their specific industry? Where do we see the trends going? What is our experience in terms of seeing what their peers are buying, from a benchmarking perspective?”

Specialized producers

Relying on the unique, in-house skills and knowledge of producers is one way for brokerages to provide specialized insurance services. One broker gave Canadian Underwriter an example of a multi-lines brokerage that employed a producer who knew a thing or two about tattoo insurance. Other examples of areas of specialization include planes, boats and checking insurance contracts.

“If you specialize in an industry, you are already walking into a meeting with information that the client may not know,” says Loeters. “Your preparation is much more focused and your time with the client is much more efficient. You need to bring value to your clients. If you meet with the executive of widget manufacturer, for example, and it takes you 20 minutes to say, ‘Let me explain a widget to you,’ that’s of no value to the client. They expect you to know that.”

Specialized brokerages

Of all of the specialization options, this may be the riskiest.

“The danger of specializing your entire brokerage is that you have to make sure you pick a field that’s broad enough that it’s not going to be disrupted by someone else coming into that market,” says Orr. “If your single product line happens to get disrupted, that’s a challenge.”

Given the hypothetical scenario of an insurance brokerage that specializes in ostrich farming, Young elaborates on the point: “There has to be a large enough volume of business to specialize,” she says. “To use your example, how many ostrich farms are there? Maybe there are only five ostrich firms in all of Montreal or in all Alberta. Maybe that’s big, but you’re probably not going to make a living on that.”

Specialized digital platform

When brokers talk about “specializing” in personal lines, they often mean distributing traditional home and auto insurance products through a fully digital brokerage. But as some brokers note, this strategy is not for everyone.

For one thing, home and auto lines are highly commoditized. The auto insurance product is highly regulated in Canada, leaving little room for variation in the auto products available for brokers to sell to consumers. Price therefore becomes a big factor in selling the personal lines auto product. In fact, brokerage owners and principals participating in our national survey identified the “price demands of customers” as the second-strongest challenge to their business (54.7%), ranking below finding qualified workers (66%).

Adam Mitchell is president of Mitchell & Whale Insurance Brokers, an Ontario-based brokerage that taps into new technologies to promote business growth. Unlike in a traditional brokerage model, a purely digital brokerage caters to a comparatively fickle type of clientele – an online world in which consumers are shopping around for a better price. For the broker, that means a higher potential for poor client retention and unprofitable risks (leading to increased loss ratios), and higher operating costs because of the technology required to run the business. On the other hand, the potential for growth is better because younger clients are increasingly using technology to do their insurance buying.

Have your say: