Reinsurance cession ratio across global P&C industry registers small rise for first time in several years: Aon Benfield

September 12, 2016 by Canadian Underwriter

Print this page Share

Reinsurance demand has increased over the past 18 months, with the cession ratio across the global property and casualty insurance industry registering a small rise for the first time in several years, according to Aon Benfield’s September 2016 edition of its Reinsurance Market Outlook report.

Released on Sunday at Aon Benfield’s Monte Carlo Rendez-Vous press conference, the report examines the current position of the industry and the outlook for the January 1 reinsurance renewals, as well as the key areas of growth for re/insurers, including property casualty, cyber, mortgage and crop businesses.

Released on Sunday at Aon Benfield’s Monte Carlo Rendez-Vous press conference, the report examines the current position of the industry and the outlook for the January 1 reinsurance renewals, as well as the key areas of growth for re/insurers, including property casualty, cyber, mortgage and crop businesses.

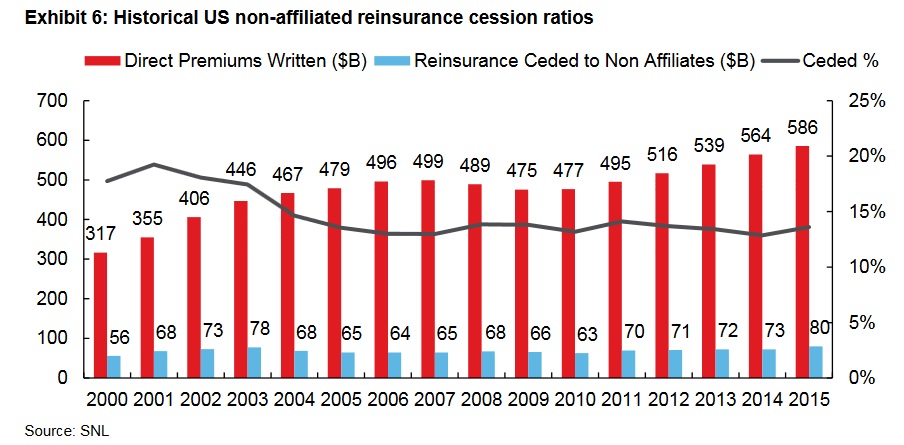

The report from Aon Benfield, the global reinsurance intermediary and capital advisor of Aon plc, said “industry data demonstrates that U.S. insurers purchased proportionately more reinsurance in 2015 for the first time in several years. This trend has continued into 2016, driven by the improved economics and multiple uses of the coverage available in the current environment,” the report noted.

“The catalysts for this increased demand for property and casualty reinsurance include factors such as the emergence of poor underwriting results in certain casualty classes, out-sized losses from regional exposures, and the introduction of the Solvency II regulatory regime across the European Union,” said Eric Andersen, CEO of Aon Benfield, in a press release.

The report highlights four key emerging areas of growth for the re/insurance industry:

- Property Catastrophe – demand for P&C protection is expected to remain relatively stable for January 2017 renewals, absent any material reinsured loss events, the release said. While certain regions affected by regulatory changes may look to secure additional capacity, overall demand change is expected to increase by approximately 5% across the market;

- Mortgage – the demand for re/insurance of mortgage default exposure in the United States continues to grow, driven by both new and existing cedents. Most of the re/insurance purchased is driven by new regulatory capital requirements, as government entities Fannie Mae and Freddie Mac continue to access private markets for credit risk transfer. To date, Aon Benfield has placed about US$10 billion of reinsurance capacity in this sector, which equates to approximately US$2.5 billion of projected lifetime ceded premium;

- Cyber – demand for cyber insurance coverage and product continues. With approximately US$1.7 billion in premium, nearly 90% of the market is based in the U.S., with annual growth running at 30-50%. International growth will be driven by upcoming European Union regulations covering data protection that will become effective in 2018.

- Crop – While a more mature market, crop re/insurance has returned to profitability in the U.S. Growth has mainly emanated from Asia, with the Indian market seeing five times the insurance premiums for the 2016/2017 season compared to the year prior. Thailand has also seen growth, albeit not as significant, Aon Benfield said in the release.

Aon Benfield estimates that global reinsurer capital rose by 4% to a new high of US$585 billion over the six months to June 30, 2016. Overall reinsurer capital has increased by more than 70% since 2008, the report pointed out.

In addition to the four key areas of growth, the report also reveals how the low interest rate environment that has persisted in the developed world since the 2007 financial crisis has had a pervasive effect on traditional re/insurance carriers that are mainly invested in cash and bonds, and has “significantly influenced market behaviour.”

Have your say: