Travelers’ net income up 9% in Q4 2016 to US$943 million

January 24, 2017 by Canadian Underwriter

Print this page Share

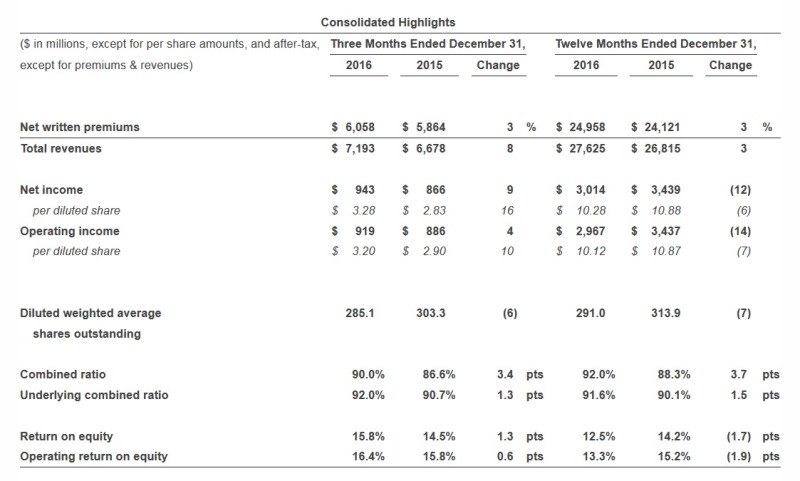

The Travelers Companies, Inc. has reported a net income of US$943 million for the fourth quarter of last year ending Dec. 31, 2016, up 9% from US$866 million in the prior-year quarter.

Travelers released its financial results on Tuesday, noting that operating income in Q4 2016 was US$919 million compared to US$886 million in Q4 2015. “These increases were primarily driven by the benefit from the settlement of a reinsurance dispute and higher net investment income, partially offset by a lower underwriting gain driven by higher catastrophe losses and higher loss estimates for personal auto bodily injury liability coverages,” Travelers said in a press release.

The combined ratio for the fourth quarter of 2016 was 90%, up 3.4 points from 86.6% in the same quarter a year earlier, due to higher catastrophe losses (1.4 points), a higher underlying combined ratio (1.3 points) and lower net favourable prior-year reserve development (0.7 points). For the 12 months ending Dec. 31, 2016, the combined ratio was 92%, up 3.7 points from 88.3% in the same period in 2015, due to higher cat losses (1.5 points), a higher underlying combined ratio (1.5 points) and lower net favourable prior-year reserve development (0.7 points).

Net written premiums (NWP) were US$6.06 billion in Q4 2016, up 3% from US$5.86 billion in the fourth quarter of 2015 and driven by Personal Insurance, Travelers said in the release. For 12M 2016, NWP were US$24.96 billion, compared to US$24.12 billion for the 12 months ending Dec. 31, 2015.

For the fourth quarter of last year, net favourable prior-year reserve development in Business and International Insurance and Bond & Specialty Insurance of US$309 million pre-tax was partially offset by net unfavourable prior-year reserve development in Personal Insurance of US$45 million pre-tax. Catastrophe losses in the fourth quarter of 2016 primarily resulted from Hurricane Matthew and wildfires in Tennessee, Travelers said.

Operating income for Travelers’ Business and International Insurance segment was US$722 million after-tax in Q4 2016, an increase of US$156 million, primarily due to the benefit of the settlement of the reinsurance dispute, a higher underlying underwriting gain, higher net investment income and higher net favourable prior-year reserve development, partially offset by higher cat losses. The combined ratio of 89% improved 0.6 points due to higher net favourable prior-year reserve development (1.5 points) and a lower underlying combined ratio (1.3 points), partially offset by higher cat losses (2.2 points). Net written premiums of US$3.45 billion decreased 1%.

For full-year 2016, operating income for Business and International Insurance was US$2.05 billion after-tax, a decrease of US$122 million, primarily driven by higher catastrophe losses, a lower underlying underwriting gain and lower net investment income, partially offset by the reinsurance settlement and higher net favourable prior-year reserve development. The combined ratio of 94.3% increased 2.2 points due to higher cat losses (1.8 points) and a higher underlying combined ratio (0.9 points), partially offset by higher net favourable prior-year reserve development (0.5 points). Net favourable prior-year reserve development primarily resulted from better than expected loss experience in the company’s domestic operations in the workers’ compensation and general liability product lines (excluding an increase to asbestos and environmental reserves), as well as in the company’s international operations in Europe and Canada, partially offset by a US$225 million pre-tax and an US$82 million pre-tax increase to asbestos and environmental reserves, respectively. NWP of US$14.7 billion increased 1%.

In Personal Insurance, operating income was US$97 million after-tax in Q4 2016, a decrease of US$125 million, primarily driven by a lower underlying underwriting gain and net unfavourable prior-year reserve development compared to net favourable prior-year reserve development in the prior year quarter, partially offset by higher net investment income. The combined ratio of 98.2% increased 11.5 points due to a higher underlying combined ratio (7.0 points), net unfavourable prior-year reserve development compared to net favourable prior-year reserve development in the prior-year quarter (4.1 points) and higher cat losses (0.4 points). Net unfavourable prior-year reserve development primarily resulted from higher-than-expected loss experience in the auto product line for bodily injury coverages in the latter part of the 2015 accident year, the release added. NWP of US$2.06 billion increased 12%. Agency Automobile NWP grew 19% with an increase in policies in force of 13% from the prior-year period, Travelers reported, adding that Agency Homeowners & Other NWP grew 3%, with an increase in policies in force of 3% from the prior-year period.

In Personal Insurance, operating income was US$97 million after-tax in Q4 2016, a decrease of US$125 million, primarily driven by a lower underlying underwriting gain and net unfavourable prior-year reserve development compared to net favourable prior-year reserve development in the prior year quarter, partially offset by higher net investment income. The combined ratio of 98.2% increased 11.5 points due to a higher underlying combined ratio (7.0 points), net unfavourable prior-year reserve development compared to net favourable prior-year reserve development in the prior-year quarter (4.1 points) and higher cat losses (0.4 points). Net unfavourable prior-year reserve development primarily resulted from higher-than-expected loss experience in the auto product line for bodily injury coverages in the latter part of the 2015 accident year, the release added. NWP of US$2.06 billion increased 12%. Agency Automobile NWP grew 19% with an increase in policies in force of 13% from the prior-year period, Travelers reported, adding that Agency Homeowners & Other NWP grew 3%, with an increase in policies in force of 3% from the prior-year period.

Full-year 2016 results for Personal Insurance showed a US$510 million after-tax operating income, a decrease of US$379 million, primarily driven by net unfavourable prior-year reserve development compared to net favourable prior-year reserve development in the prior year, a lower underlying underwriting gain and higher cat losses. The combined ratio of 95.1% increased 8.5 points due to net unfavorable prior-year reserve development compared to net favorable prior year reserve development in the prior year (4.3 points), a higher underlying combined ratio (3.3 points) and higher cat losses (0.9 points). According to Travelers, net unfavorable prior-year reserve development primarily resulted from higher than expected loss experience in the auto product line for bodily injury coverages in the latter part of the 2015 accident year. NWP of US$8.18 billion increased 10% due to the same factors discussed above for the fourth quarter of 2016.

Alan Schnitzer, Travelers’ CEO, said in the release that “in our commercial businesses, we continue to be pleased with the stability of the markets in which we operate and the execution of our strategies. Once again, we were able to maintain historically high levels of retention while achieving stable and positive renewal premium change. These results demonstrate the continued success of our granular pricing and segmentation strategies – retaining those accounts that meet our return thresholds and taking appropriate measures to improve profitability on those accounts that do not, while seeking attractive new business opportunities.”

Within Personal Insurance, both homeowners and auto delivered accelerating growth in policies in force and NWPs throughout the year, Schnitzer said. “While homeowners profitability remains strong, we are disappointed with the underwriting results in personal auto and are taking pricing and other actions to improve its profitability.”

Have your say: