Understanding potential disruptions to risk analysis, cost basis and distribution key to insurers’ strategies: Novarica

September 22, 2016 by Canadian Underwriter

Print this page Share

Insurers need to understand potential disruptions to risk analysis and cost basis as well as distribution to effectively manage their strategies, suggested a new report from Boston-based research and advisory firm Novarica.

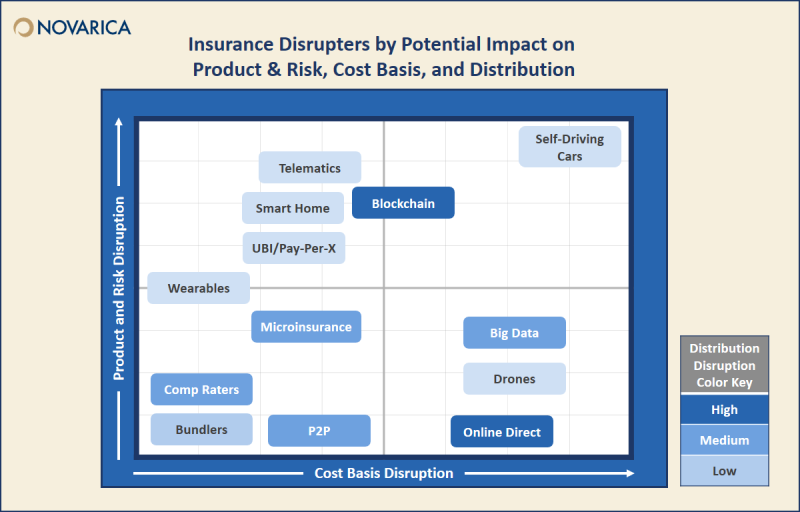

The pace of technological change makes it a daunting task for insurers, many of whom are still managing legacy systems, to understand which emerging technologies represent a true disruptive threat to their business model, Novarica said in the report Understanding Insurance Disrupters. The report, released on Tuesday, reviews 13 categories of disruption – from online direct sales to wearable devices to self-driving vehicles – to help insurer chief information officers understand the marketplace, Novarica said in a statement.

The pace of technological change makes it a daunting task for insurers, many of whom are still managing legacy systems, to understand which emerging technologies represent a true disruptive threat to their business model, Novarica said in the report Understanding Insurance Disrupters. The report, released on Tuesday, reviews 13 categories of disruption – from online direct sales to wearable devices to self-driving vehicles – to help insurer chief information officers understand the marketplace, Novarica said in a statement.

“Insurers that don’t adopt emerging technologies are going to face declines as their agents and customers become intolerant of their poor capabilities and competitors improve their risk analysis and cost bases,” said Jeff Goldberg, vice president of research and consulting and lead author of the report. “That being said, most disruption isn’t going to signal the end of the current industry model. Investing in disruptive technologies isn’t for everyone, and for the most part, the old and the new can coexist. The goal for all insurers should be to understand new challenges and make strategic choices rather than let the market choose for them, and that’s exactly where this report is designed to help.”

According to the report, product and risk disrupters such as telematics and microinsurance mean new and expanded offerings to the marketplace, “but this does not necessarily replace existing lines. Insurers should make sure they think of their products in terms of what can be, not what was,” the report advised.

Cost basis disrupters, like drones and big data, streamline processes and lower costs and in some cases, they will adjust long-term loss profiles, the report said. “Insurers should make sure they understand how competitors will use these cost advantages to underprice them.”

Cost basis disrupters, like drones and big data, streamline processes and lower costs and in some cases, they will adjust long-term loss profiles, the report said. “Insurers should make sure they understand how competitors will use these cost advantages to underprice them.”

Distribution disrupters, like online direct and blockchain, change how insurers sell; many approaches will thrive in an omni-channel world. “Insurers should make sure they observe how customers actually want to buy, and not just what their current distributers prefer,” the report suggested.

“One common refrain about technology when it comes to emerging technology is ‘adapt or die,’” the report said. “Unfortunately, the urgency in this statement is misleading. Legacy systems are not a Y2K problem – there’s no ticking time bomb. And legacy systems or not, it takes an insurance company a long time to die.”

Novarica argued that a more accurate, but perhaps less catchy slogan might be “adapt or decline. Without digital channels, effective data analytics and agile core systems, insurers will face declines. Their agents and customers will first tolerate and then resent their poor communication capabilities. Their actuaries, underwriters and claims adjusters will start to underperform int eh market for lack of data and analytical capabilities. Their product freshness will grow stale compared to more agile peers as core systems inhibit speed to market.”

Have your say: