Autonomous vehicles may reduce U.S. motor premiums by more than 40% by 2050: Aon Benfield

September 13, 2016 by Canadian Underwriter

Print this page Share

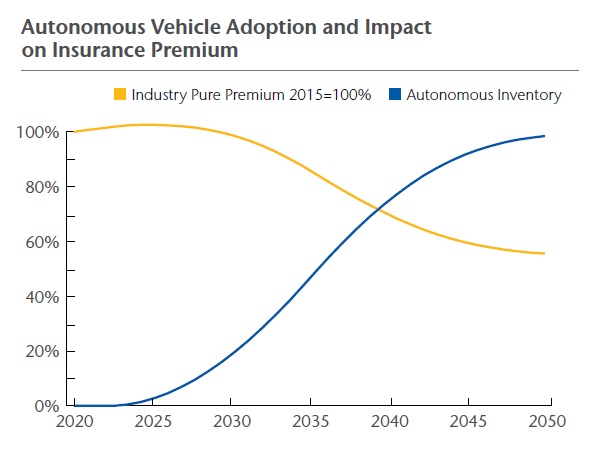

Autonomous vehicles may reduce motor pure premiums in the United States by more than 40% by the time they “reach full adoption in 2050,” according to a recent Global Insurance Market Opportunities report from Aon Benfield.

Aon Benfield, the global reinsurance intermediary and capital advisor of Aon plc, released the report on Sunday. Titled Riding the Innovation Wave, the report – now in its 11th edition – examines the key areas of potential growth and disruption for insurers.

According to the study, if autonomous vehicle technology is adopted “at even a moderate pace,” U.S. motor pure premiums could decrease by 20% by the year 2035 compared to their 2015 levels – and potentially by more than 40% by the time they reach full adoption in 2050.

“Yet for the insurance industry, these risks also present opportunities for growth if the right combination of capital plus data and analytics can be brought to bear,” the report said. “Even autonomous vehicles may have an insurance upside, as the decline in personal motor premiums could be partially offset by a rise in premiums for the car manufacturers and the technology companies on whose networks the driverless vehicles operate.”

With the first commercially available technology expected to hit the road in 2018, the forecast assumes an 81% reduction in claims frequency, and an increase in claims severity due to sensor costs and an increased cost of handling product liability claims.

Personal motor accounts for 47% of global insurance premium – without this ballast and implicit capital subsidy, Aon Benfield estimates that U.S. property-casualty insurance volatility could increase by 40%, Aon Benfield said in a press release.

“Adoption of autonomous vehicles will of course be affected by many variables, such as regulatory challenges, cost to the consumer, safety, vehicle ownership preferences and the technology itself,” Paul Mang, CEO of Aon Analytics, said in the release. “However, we as an industry need to act quickly to ensure that we have the products available to align to the new paradigm; if we fail to do so, we only invite disruption.”

“Adoption of autonomous vehicles will of course be affected by many variables, such as regulatory challenges, cost to the consumer, safety, vehicle ownership preferences and the technology itself,” Paul Mang, CEO of Aon Analytics, said in the release. “However, we as an industry need to act quickly to ensure that we have the products available to align to the new paradigm; if we fail to do so, we only invite disruption.”

In terms of opportunities, if the current pace of growth is maintained, Aon Benfield forecasts that by 2020 global cyber premiums could reach US$10 billion – a figure at least as large as the worldwide directors’ and officers’ liability market. In fact, the Global Council on Internet Governance has forecast that cybercrime could grow to US$2-3 trillion by 2020 – equivalent to the GDP of a top 10 economy, the release said.

In terms of potential disruption, the report reveals that in 2015 there was US$2.6 billion of investment across more than 200 insurance startups, part of US$9 billion invested in the sector in the past several years globally. “Venture capitalists are not interested in our industry in its current form; they are aiming to reorganize our processes and operations in order that they can create new economic opportunities for themselves,” Mang added.

The Global Insurance Market Opportunities report also suggested that insurers should perform a careful examination of their own value chain, with the aim of evaluating core strengths and identifying weaknesses. Firms should also think carefully about how data and analytics can be applied to serving clients and reorganizing core operations.

Have your say: