Incumbent insurers should rethink businesses, embrace opportunity in digital technology: McKinsey & Company

March 9, 2017 by Canadian Underwriter

Print this page Share

The insurance industry is not impregnable and companies would be well-advised to reinvent themselves by incorporating digital technology and allowing it to become a catalyst, suggests a new report issued Thursday by McKinsey & Company.

Some executives “know that staying competitive in a digital world will require far more than the addition of a direct sales channel or a few automated processes,” notes the report, Digital disruption in insurance: Cutting through the noise.

Some executives “know that staying competitive in a digital world will require far more than the addition of a direct sales channel or a few automated processes,” notes the report, Digital disruption in insurance: Cutting through the noise.

McKinsey & Company argues that what seems to be needed is “a fundamental rethink of the corporation, for which digital technology is but the catalyst.”

Companies must rethink the sources of revenue and efficiency, the organizational and talent model and, ultimately, “the business model and the role they will play in an ecosystem that cuts across traditional industry boundaries,” states the report.

So far, “insurance has been relatively slow to feel the digital effect owing to regulation, large in-force books, and the fact that newcomers seldom have the capital needed to take insurance risk on to their balance sheets,” it explains.

“Companies that fail to adapt will weaken under the pressure exerted by those that use digital technology to slash costs and get better returns on their investments,” it adds.

“Already, in personal auto insurance, we see how sensors fitted in vehicles will be likely to put premiums under pressure as driving becomes safer,” the report points out.

Customer demands, clearly, are changing. Among those demands are simplicity through one-click shopping; 24-hour access and quick delivery; clear, relevant information about a product’s features, particularly in relation to pricing; and innovative, tailored services designed for the digital age.

Customer demands, clearly, are changing. Among those demands are simplicity through one-click shopping; 24-hour access and quick delivery; clear, relevant information about a product’s features, particularly in relation to pricing; and innovative, tailored services designed for the digital age.

But the report strongly recommends insurers should view these changing demands as an opportunity to get closer to customers.

“Digital technology and the data and analysis it makes available give insurers the chance to know their customers better,” the report notes. “That means they can price and underwrite more accurately, and better identify fraudulent claims.”

In the longer term, “growth opportunities reside in innovative insurance products and protection services,” McKinsey & Company expects. These include cyber security offerings to help prevent and protect against the breach or loss of data and damage that might ensue, and products related to the sharing economy.

“Data from connected devices can be used to assess risk more accurately. But it is also a powerful tool to lower risk – to prevent accidents in the home, reduce maintenance and downtime or improve health,” the research points out.

“This logically leads to a model whereby consumers pay not for premiums in order to be compensated for damages they might incur, but for gadgets or services that predict and help prevent that risk,” the company predicts.

In moving forward with technology is also the potential for savings. Automation can reduce the cost of a claims journey by as much as 30%, the report states.

McKinsey & Company “estimates that up to 40% of p&c and life insurers’ expenses are locked up in their top 20 to 30 core end-to-end processes – costs that digitization can reduce, and in some cases, eliminate.”

Looking at auto specifically, “by digitizing existing business, our research suggests, a large incumbent could more than double profits over the course of five years,” the report notes.

In the longer term, “earnings from traditional business will face headwinds as driving becomes less risky owing to the use of sensors and telematics or because, in the case of autonomous cars, liability is transferred to manufacturers. Fifteen years on, profits for traditional personal lines auto might fall by 40% or more from their peak,” the report adds.

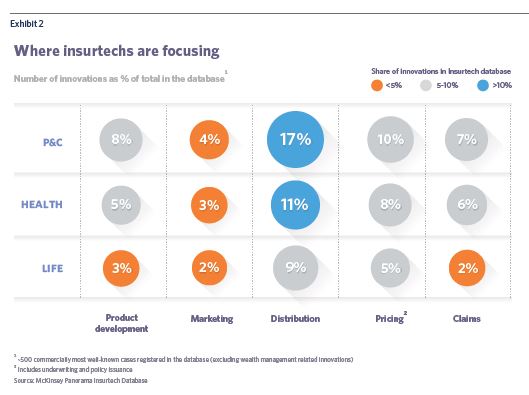

Add to this mix the increasing influence of insurtechs. “They are not about to overturn today’s value chain, but there are longer-term trends afoot that might,” the report notes.

The research suggests insurers are threatened by three trends:

- a shift toward preventing risk rather than insuring against it;

- the increasing power of those companies that own and analyze data; and

- the investment of huge amounts of capital in insurance-related capital market instruments by institutional investors seeking high returns.

For more than a decade, institutional investors “have focused mainly on reinsuring property catastrophe risk – a sum of US$70 billion in 2015. But now they have their eyes on the primary market,” the report maintains.

“Venture capitalists globally invested US$2.6 billion in insurtechs in 2015, and nearly US$1.7 billion in 2016,” McKinsey & Company notes.

“Although these newcomers are populating every part of the value chain, their focus to date has been on the more easily accessible slivers of the industry – mainly distribution, particularly in p&c insurance,” it points out.

The traditional insurance business model has proved to be remarkably resilient, states the report, but it is starting to feel the digital effect.

That said, positives remain for insurers. “Regulation, product complexity and insurers’ large balance sheets have kept digital attackers from insurers’ gates. That is changing, but in ways incumbents should embrace,” the report emphasizes.

That said, positives remain for insurers. “Regulation, product complexity and insurers’ large balance sheets have kept digital attackers from insurers’ gates. That is changing, but in ways incumbents should embrace,” the report emphasizes.

“We firmly believe that opportunities abound for incumbent insurance companies in this new world. But they will not be evenly shared,” McKinsey & Company cautions.

“Those companies that move swiftly and decisively are likely to be those that flourish. Those that do not will find it increasingly challenging to generate attractive returns,” the company adds.

“Incumbents have the advantage of large capital reserves, as start-ups seldom want to take risk on to their balance sheets because of the capital they need to offset it,” the report states. In addition, incumbents “have the advantage of underwriting skills built on years of experience and proprietary data.”

Though insurers have valuable historic data, “in a few years’ time, will they be able to keep pace and still add underwriting value when competing with newcomers that have access to more insightful, often real-time new data culled from the Internet of Things (IoT), social media, credit card histories, and other digital records?”

Properly managing a successful digital transformation – which could take as long as a decade, requires answering a number of questions, including the following:

Properly managing a successful digital transformation – which could take as long as a decade, requires answering a number of questions, including the following:

- Where should the company start – with cost-cutting or growth initiatives?

- Is it necessary to rip out IT systems and start again?

- Should a new, digital unit be established? If so, will it cannibalize other business?

- How can the company attract the new talent that will be needed?

A McKinsey & Company survey of more than 2,000 executives in industries affected by digital technology indicates “the companies with the highest revenue and earnings growth looked for digital opportunities across all elements of their business model, not just one or two, and either led the disruption or were fast followers.”

These leaders “made bets on digital processes across the value chain, on innovative products, and on new business models,” it adds.

The report argues success will be grounded in recognizing the drivers of value in a digital age, namely: technological leadership and innovation; customer ownership; efficiency (cost savings) and effectiveness (higher returns); scale and network effects; and speed and agility.

Related: U.S. financial firms looking to robo-technology to complement existing service models

Have your say: