Insurance agency M&A in Canada and U.S. in 2016 second-highest recorded: study

February 1, 2017 by Canadian Underwriter

Print this page Share

Mergers and acquisitions (M&A) of insurance agencies last year were the second-highest ever in 2016 at 449 deals in Canada and the United States, a slight dip from the all-time record of 456 in 2015, according to OPTIS Partners’ annual report.

Insurance agency mergers and acquisitions, US and Canada, by buyer type, 2008-2016. Source: OPTIS Partners.

The report was released on Tuesday by the Chicago-based OPTIS, an investment banking and financial consulting firm specializing in the insurance industry. It is focused exclusively on the insurance distribution marketplace and offers M&A representation for buyers and sellers, including due diligence reviews.

“It was a sellers’ market last year, and it will probably remain one in 2017,” said Timothy J. Cunningham, managing director of OPTIS, in a press release. “But the perfect storm benefitting sellers won’t last forever.”

The report covered reported transactions of agencies selling primarily property and casualty insurance, agencies selling both P&C and employee benefits and employee benefits agencies. According to the report, private equity-backed agencies were 2016’s biggest buyers, making 237 purchases, 53% of the total. The top two were Acrisure (63 deals) and Hub International (45 deals), the release pointed out. Privately owned insurance agencies came in second, buying 124 agencies. They were followed by public brokers (41), banks (25) and carriers/other (22).

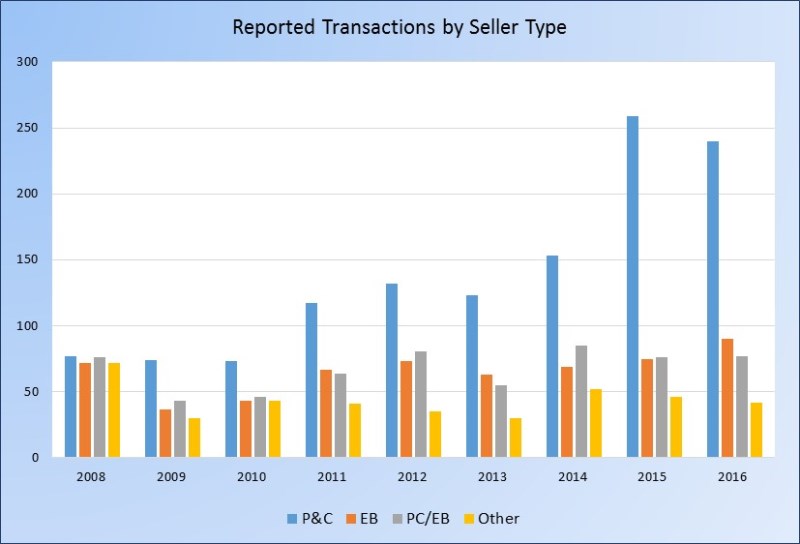

Looking at sellers, sales of P&C-focused agencies continue to dominate the list, with 54% of all sales, OPTIS reported. Sales of employee benefits agencies rose to become the second most popular category, accounting for 20% of sales, up from 17% in 2015. Deals for both agencies selling both P&C and employee benefits held steady at 17% of transactions. The “other” category was 9%.

Insurance agency mergers and acquisitions, US and Canada, by seller type, 2008-2016. Source: OPTIS Partners.

OPTIS partner Daniel P. Menzer said that the statistics pointed to several key lessons:

- Valuation pricing is driven by the underlying value of the business and by market competitive forces, both of which have many contributing factors;

- Buyers, in particular smaller and less capitalized firms, need to be careful not to get carried away in the pricing competition for a seller’s business only to find out later they can’t afford to pay for it;

- Firms wrestling with trying to perpetuate need to be steadfast in setting realistic valuations for internal transactions without getting overly swayed by actual and anecdotal pricing stories of other agency transactions; and

- For agency owners waiting for the “right time to sell” before jumping on the bandwagon, now is the right time.

Cunningham noted that the actual number of sales was even greater than the 449 reported, as many buyers and sellers do not report transactions, and some acquirers do not report small transactions. “The OPTIS database tracks a consistent pool of the most active acquirers, including other announced deals, and is, therefore, a reasonably accurate indication of deal activity in the sector,” he said.

Have your say: