Link between oil price reduction, increase in major incidents: Marsh

March 24, 2016 by Canadian Underwriter

Print this page Share

Energy firms are facing challenges, including falling revenues, but are encouraged to maintain their investment in risk management to reduce the potential for future major incidents and insurance claims, suggests a new research report from global insurance broker and risk advisor Marsh.

Over the past 20 months, oil prices have fallen by about 70%, notes Can Energy Firms Break the Historical Nexus Between Oil Price Falls and Large Losses?, released this week at the firm’s bi-annual National Oil Companies conference in Dubai.

Over the past 20 months, oil prices have fallen by about 70%, notes Can Energy Firms Break the Historical Nexus Between Oil Price Falls and Large Losses?, released this week at the firm’s bi-annual National Oil Companies conference in Dubai.

In the upstream market, the report notes that periods of significant pricing falls historically have been met by the following:

- new projects being shelved or cancelled;

- increase in redundancies and hiring freezes;

- cuts in infrastructure and maintenance spending; and

- less investment in health and safety measures and employee training.

“Already, companies have been cancelling projects and making staffing reductions,” states the report, which analyzes the historical sequential correlation between oil price reductions, which led to energy firms cutting costs, including safety training and education, which, in turn, led to an occurrence of significantly larger insured losses in the following period.

“It is estimated that projects worth up to US$380 billion have been shelved, according to consultancy group Wood Mackenzie,” Marsh points out.

“While project cancellations and redundancies are easy to quantify due to publicly available information, cuts in maintenance, health and safety measures, and employee training are far more difficult to assess. With a prolonged period of low oil prices expected, however, the question now is when oil and gas companies begin spending less on maintenance and health and safety,” the reports notes.

“Analysis of past cycles indicates that cost-cutting decisions were followed by an increased frequency of major incidents or large losses,” Andrew George, chairman of Marsh’s Global Energy Practice, says in a statement from Marsh, a wholly owned subsidiary of Marsh & McLennan Companies, Inc.

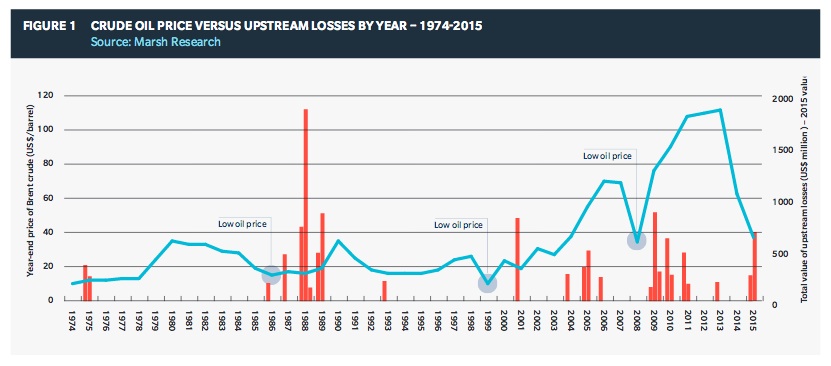

Marsh points out that insured losses in the global upstream energy sector reached a peak in the 1980s, shortly after the price of Brent crude oil fell from US$35 to US$15 per barrel. This cycle also occurred in the late 1990s, when the price fell below US$10 per barrel, and in the years following the 2008 slump, when the price fell from more than US$100 to US$32 per barrel. [click image below to enlarge]

“Signs in the market point to oil and gas prices remaining low for an extended period of time,” the report states. Given this new environment, the following issues are likely to unfold:

- new projects becoming smaller, cheaper, and quicker (multibillion-dollar projects are likely to decrease, with more projects falling in the US$50 million to US$100 million cost range becoming more common);

- exploration drilling projects in new regions such as the Arctic will largely be put on hold, as the cost of extraction versus the market price of oil render this commercially unviable; and

- merger and acquisition activity will likely increase as the number of attractively priced energy assets increase.

Related: Oil-dependent economies, including Canada, among countries placed on negative watch list: Coface

With less revenue and more strain on budgets, the report cautions that “companies could find themselves challenged to face future volatility should it arise, which could be driven by reduced demand and supply issues,” including a drive towards greener energy production and improved technology reducing consumption patterns.

“Firms that have invested in risk management have seen real benefits,” George maintains. “Energy companies should exercise caution when implementing cost-cutting measures in response to this latest downturn to avoid a repetition of the major losses that occurred in the past,” he cautions.

Marsh further points out that opportunity exists for insurers to be more innovative in the products they are offering to generate more interest from energy companies. These relate to the following:

- cyber (with the remote use of supervisory control and data acquisition, or SKADA, systems in the oil and gas sectors, few policies offer coverage for cyber risks or the possibility for resulting physical damage);

- simplified loss of revenue products to aid insurance buyers for whom this is becoming a growing concern;

- credit risk, as clients look to protect receivables; and

- directors and officers (D&O) liability insurance as a result of fears of litigation and claims from shareholders as profits collapse.

Related: Higher demand for p&c coverage a possible silver lining of depressed oil prices: AGCS

For companies, the opportunity clearly exists “to access cheap sources of capital from the insurance markets, reduce overall insurance premium costs, purchase insurance in areas that were previously omitted due to cost, and renegotiate coverage terms,” the report states. “Now would appear the time to transfer risk off their balance sheets before volatility increases,” it recommends.

“Organizations that take a more forward-looking approach, re-evaluate their risk appetite and tolerance, and use the energy insurance market to transfer greater amounts of risk off their balance sheets will likely be in a stronger position over the longer term,” the report adds.

Have your say: