Reduced market access, regulatory fragmentation and cloud risk accumulation among key industry risks: Swiss Re

June 13, 2017 by Canadian Underwriter

Print this page Share

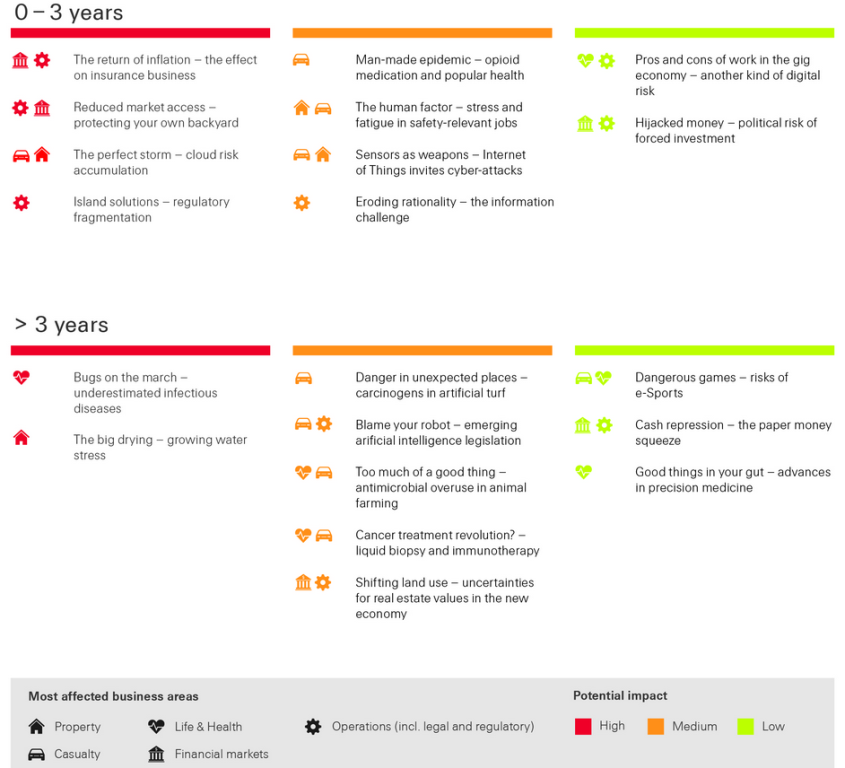

Reduced market access, regulatory fragmentation, the return of inflation, cloud risk accumulation and emerging liability legislation for artificial intelligence are just some of the key risks for the re/insurance industry, according to Swiss Re’s 2017 SONAR report.

The report, released on Tuesday, is based on “the SONAR process, a crowdsourcing tool drawing on Swiss Re’s unique internal risk management expertise to pick up early signals of what lies beyond the horizon,” the reinsurer said in a statement.

The report, released on Tuesday, is based on “the SONAR process, a crowdsourcing tool drawing on Swiss Re’s unique internal risk management expertise to pick up early signals of what lies beyond the horizon,” the reinsurer said in a statement.

The report offers insights into emerging risks and highlights a number of emerging trend spotlights. Emerging risks are newly developing or evolving risks that are difficult to quantify and sometimes not fully understood, but potentially have an impact on the industry and society, Swiss Re explained. Emerging trend spotlights examine early development, which may offer both opportunities and risks for the insurance industry in the future. The report features 20 new emerging risk themes and six emerging trend spotlights.

Swiss Re said the “six top risks with the highest potential impact” are:

- Reduced market access – The use of regulation to control capital flows and encourage protectionism could eventually undermine the business models of international corporations;

- Regulatory fragmentation – Increased fragmentation in regulation could undermine re/insurers’ ability to support economic activity and act as stabilizers in the financial markets. In a fragmented regulatory world, there is also much less opportunity to efficiently pool risks;

- The return of inflation – After years of low inflation and even fears of deflation, we see signs of headline price increases here and there. Inflation can affect insurers’ profitability, in particular on long-term liabilities (life, casualty). It can also have an adverse impact on asset management;

- Cloud risk accumulation – Cloud services have become widespread, for business and households alike. But as the cloud accumulates data-sets and services on an ever-increasing scale, it also generates a variety of risks that may accumulate to a “perfect storm”, for example by a cyberattack or power blackout, Swiss Re said;

- Growing water stress – While the Southwest portion of the United States is in an ongoing water crisis, similar situations can be found “today and in the future” around the world, from southern Europe and the Mediterranean to Africa, parts of Asia and Latin America. The risks range from wildfires, competition for water among the energy and agricultural sectors to mass migration and wider conflict potentials; and

- Underestimated infectious diseases – The question is not whether deadly infectious diseases will appear, but when and how society is prepared to cope with them. In an extreme scenario, each epidemic or pandemic has high relevance for life and health insurance and the financial markets.

“Ignoring emerging risks is not an option, neither for political decision-makers, the insurance industry, nor society as a whole,” said Patrick Raaflaub, Swiss Re Group’s chief risk officer, in the statement. “The earlier we adapt to these changes, the better prepared we will be. Sharing knowledge through a proactive risk dialogue across stakeholders can help the insurance industry create a proactive and pre-emptive risk management culture that enables disciplined risk-taking. That is an important step to help society as a whole to become more resilient,” he argued.

“Ignoring emerging risks is not an option, neither for political decision-makers, the insurance industry, nor society as a whole,” said Patrick Raaflaub, Swiss Re Group’s chief risk officer, in the statement. “The earlier we adapt to these changes, the better prepared we will be. Sharing knowledge through a proactive risk dialogue across stakeholders can help the insurance industry create a proactive and pre-emptive risk management culture that enables disciplined risk-taking. That is an important step to help society as a whole to become more resilient,” he argued.

The identified risks are relevant to life and non-life insurance areas, as well as asset management, Swiss Re explained. They are presented with the goal of helping industry players prepare for new scenarios by adapting their behaviour, market conduct and product portfolios.

Have your say: