The tough calls broker, insurers will be making this year

January 25, 2021 by Adam Malik

Print this page Share

Pressure on insurers to provide sustainable results, brokers expanding their service offerings and the growing gap between big and small are just some of the trends the P&C insurance industry will face this year that will give leaders plenty to think about, predicts by an industry expert.

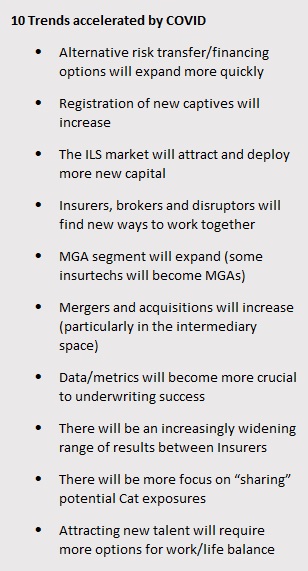

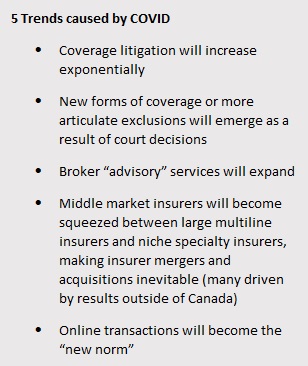

In his annual presentation looking at the top trends of the upcoming year, Phil Cook, chairman of Omega Insurance Holdings, gave a total of 20 trends that he expects to happen — 10 that have been accelerated by the pandemic, five that have been caused by COVID-19 and five that are coming no matter what. (See sidebars for full list.)

Industry Trends & Predictions: 2021 was held virtually this year by the Insurance Institute of Ontario due to the pandemic.

In a trend that was unrelated to the COVID-19 pandemic, Cook stressed that insurers will face pressure to produce sustainable results, which was going to happen whether or not the world changed last March as results at the end of 2019 were already not sustainable and unattractive to investors.

In a trend that was unrelated to the COVID-19 pandemic, Cook stressed that insurers will face pressure to produce sustainable results, which was going to happen whether or not the world changed last March as results at the end of 2019 were already not sustainable and unattractive to investors.

“And that that will continue. We have to get back to those sustainable results,” he observed. “Hopefully, the curve will get [combined ratios] down below that 100%, and the rate of return on invested capital and surplus will be up in that seven-plus range, which is a threshold for a lot of investors.”

In a trend that has been accelerated by COVID, mergers and acquisitions are predicted to increase this year and, perhaps relatedly, the P&C industry is going to see the gap between big and small widen even further.

In a trend that has been accelerated by COVID, mergers and acquisitions are predicted to increase this year and, perhaps relatedly, the P&C industry is going to see the gap between big and small widen even further.

When looking at industry averages for results, Cook noted, you don’t see many companies that are actually in that average range — they’re usually at either end of the spectrum. Add in the past year and the spread may become even more dramatic, not to mention creating an increasingly unstable environment.

“And that doesn’t make for very stable underwriting when you’ve got a large number of companies making a significant amount of money because their combined ratios are very low and a number of insurers making no money and losing a significant amount because their ratios are higher,” Cook said. “There has to be some way in which that those results will come closer together. In an industry of our size, there should be more companies that are within 10% of the average consistently to become a stable market.”

Similarly — though this is a trend that Cook says is caused by COVID-19 — he expects the middle market (both insurer and broker) will face challenges. Do they get bigger and compete with those at that higher level? Or do they stay small and go after the niche market? The pandemic has made that debate even more important.

Similarly — though this is a trend that Cook says is caused by COVID-19 — he expects the middle market (both insurer and broker) will face challenges. Do they get bigger and compete with those at that higher level? Or do they stay small and go after the niche market? The pandemic has made that debate even more important.

“I think domestic companies in Canada will also be looking at some acquisitions, so they can resolve that middle-market situation of, ‘Do we get bigger, or do we get smaller?’” Cook predicted.

In another trend caused by COVID-19, he sees brokers expanding the advisory services they provide. Brokers are no longer just someone to help clients find coverage, but they’re now also professors, social activists, helpers and more, Cook said, calling it a “healthy” evolution of the broker-client relationship.

“And I think if brokers were concerned about not [being] perceived as not giving up value for the commission, I think, that is about to turn around for the ones that are able to provide that sort of assistance, handholding advice and direction for their clients.”

Feature image by iStock.com/akindo

Have your say: