Economical Insurance gross written premiums up 4.8% in Q4 2016 to $521.8 million

February 22, 2017 by Canadian Underwriter

Print this page Share

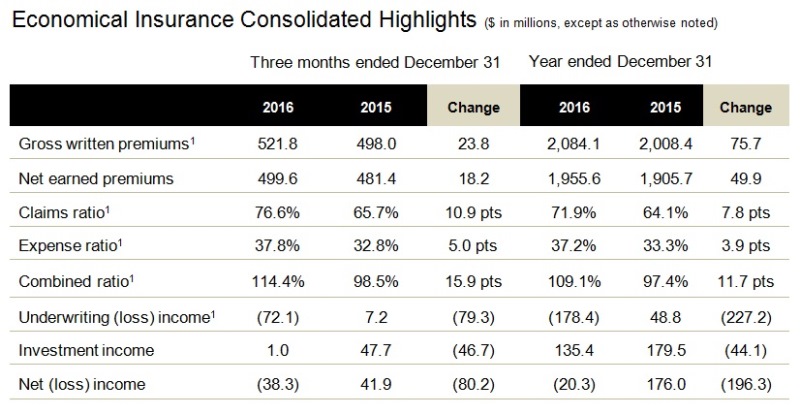

Economical Insurance has reported that gross written premiums (GWP) for the fourth quarter of 2016 ending Dec. 31 grew by $23.8 million, or 4.8%, to $521.8 million from $498 million in Q4 2015.

In particular, personal lines premiums grew by $28.3 million, or 9.5%, driven primarily by increased auto policy volumes in the insurer’s broker channel and the launch of Sonnet, its online direct channel. Commercial lines premiums declined by $4.5 million, or 2.2%, over the same quarter a year ago, Economical said in a press release on Wednesday. Excluding the earlier renewal date of certain large accounts in the third quarter of 2016, commercial lines premiums increased by $7.4 million, or 3.7%, “due to targeted rate increases for commercial property and liability, and increased fleet business.” For the year, personal lines premiums grew by $68.8 million (or 5.5%) and commercial lines premiums grew by $6.9 million (or 0.9%) over the prior year.

In particular, personal lines premiums grew by $28.3 million, or 9.5%, driven primarily by increased auto policy volumes in the insurer’s broker channel and the launch of Sonnet, its online direct channel. Commercial lines premiums declined by $4.5 million, or 2.2%, over the same quarter a year ago, Economical said in a press release on Wednesday. Excluding the earlier renewal date of certain large accounts in the third quarter of 2016, commercial lines premiums increased by $7.4 million, or 3.7%, “due to targeted rate increases for commercial property and liability, and increased fleet business.” For the year, personal lines premiums grew by $68.8 million (or 5.5%) and commercial lines premiums grew by $6.9 million (or 0.9%) over the prior year.

The overall combined ratio for the fourth quarter of 2016 was 114.4%, up 15.9 points from 98.5% in Q4 2015 and “heavily impacted by a deterioration in auto performance.” For the full year of 2016, the combined ratio was up 11.7 points to 109.1% from 97.4% in 2015.

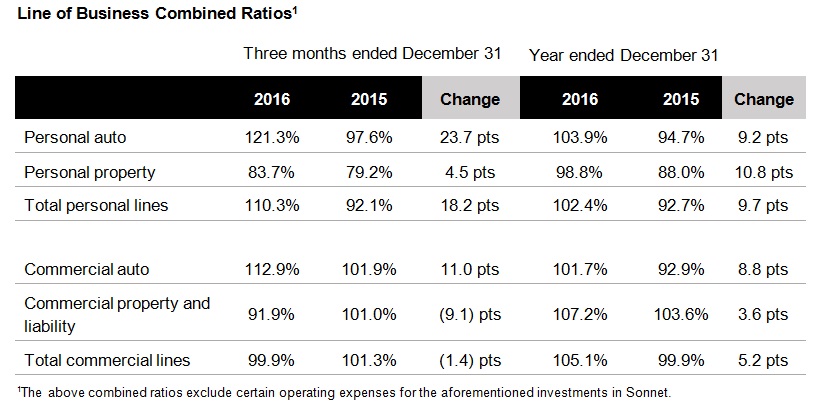

By line of business combined ratio, the personal auto combined ratio for the quarter was 121.3% in Q4 2016, “significantly impacted by a deterioration in Ontario, British Columbia and Alberta,” Economical said in the release. The Q4 2015 combined ratio was 97.6%, while the full-year 2016 combined ratio was 103.9% compared to 94.7% in 2015. “During the quarter, reserves were strengthened as a result of the ongoing trends we are seeing in this line of business,” Economical reported. “To address the challenges in personal auto, we are implementing a number of measures including improvements in pricing, underwriting and claims actions.”

The personal property combined ratio, while continuing to be strong at 83.7%, increased 4.5 points from 79.2% in Q4 2015, due to higher catastrophe losses, partially offset by higher average premiums. The personal property combined ratio was 98.8% in 2016, from 88% in 2015. Personal property for the year was significantly impacted by increased catastrophe losses, including the Fort McMurray wildfire, which had an incremental impact of 10.5 percentage points on the claims ratio. The insurer incurred net catastrophe losses of $79.9 million inclusive of reinstatement premiums and the impact of the Fort McMurray wildfire.

Overall, personal lines produced an underwriting loss of $32.9 million compared to underwriting income of $24 million in the same quarter a year ago. For the year, personal lines produced an underwriting loss of $29.7 million compared to an underwriting profit of $86.5 million in 2015. Total personal lines’ combined ratio was 110.3% in the most recent quarter, up 18.2 points from 92.1% in Q4 2015. For 2016, the total personal lines’ combined ratio was up 9.7 points to 102.4% from 92.7% in 2015.

Overall, personal lines produced an underwriting loss of $32.9 million compared to underwriting income of $24 million in the same quarter a year ago. For the year, personal lines produced an underwriting loss of $29.7 million compared to an underwriting profit of $86.5 million in 2015. Total personal lines’ combined ratio was 110.3% in the most recent quarter, up 18.2 points from 92.1% in Q4 2015. For 2016, the total personal lines’ combined ratio was up 9.7 points to 102.4% from 92.7% in 2015.

The commercial auto combined ratio was impacted in the fourth quarter of 2016 by a deterioration in Ontario due to higher claims severity and an increase in claims frequency, partially offset by lower large losses, Economical reported. The commercial auto combined ratio was 112.9% for the fourth quarter of 2016, up 11 points from 101.9% in the fourth quarter of 2015. For the year, the commercial auto ratio increased 8.8 points to 101.7% from 92.9% in 2015.

Economical also pointed out that the commercial property and liability combined ratio decreased due to lower large losses and a decrease in claims frequency and severity. Commercial property and liability was impacted by increased catastrophe losses, including the Fort McMurray wildfire, which had an incremental impact of 2.9 percentage points. This was somewhat offset by the beneficial impact of increased rate resulting from our underwriting and pricing actions, the release said. The commercial property and liability combined ratio decreased 9.1 points in the most recent quarter to 91.9% from 101% in the prior-year quarter. For the year, the commercial property and liability increased 3.6 points to 107.2% from 103.6% in 2015.

Overall, commercial lines produced a slight underwriting profit of $0.1 million compared to an underwriting loss of $2.4 million in the same quarter a year ago, Economical said. For the year, commercial lines produced an underwriting loss of $36.4 million compared to underwriting income of $1.5 million in 2015. Total commercial lines’ combined ratio was 99.9%, down 1.4 points from 101.3% in Q4 2015. For the year, the combined ratio was up 5.2 points to 105.1% from 99.9% in 2015.

Net income decreased from a profit of $41.9 million in 2015 to a loss of 38.3% million in the most recent quarter. Net income for the year decreased from a profit of $176 million in the prior year to a loss of $20.3 million in 2016. These declines were due to weaker underwriting performance, higher levels of catastrophe losses, increased spend on strategic initiatives and a decline in investment income, partially offset by a more favourable effective tax rate, Economical said.

Net income decreased from a profit of $41.9 million in 2015 to a loss of 38.3% million in the most recent quarter. Net income for the year decreased from a profit of $176 million in the prior year to a loss of $20.3 million in 2016. These declines were due to weaker underwriting performance, higher levels of catastrophe losses, increased spend on strategic initiatives and a decline in investment income, partially offset by a more favourable effective tax rate, Economical said.

“2016 was a mixed year for Economical,” said Rowan Saunders, the company’s president and CEO, in the release. “We significantly progressed key elements of our strategy including launching Sonnet, the advancement of the demutualization process, and the acquisition of Western Financial Insurance Company, closed on Jan. 1, 2017.”

“However, our fourth quarter and full year operating performance was unsatisfactory and disappointing, notwithstanding the impact of the significant investments we have made in our infrastructure and advancing our strategy,” he continued. Besides improvements in pricing, underwriting and claims actions to address the challenges in personal auto, Saunders reported that the insurer is also “heavily investing in the replacement of the personal lines policy administration system to support our broker distribution channel, which we expect will improve operating performance over the longer term, once implemented.”

Have your say: