More than half of polled P&C insurers aware of implications and potential of blockchain: Strategy Meets Action

November 11, 2016 by Canadian Underwriter

Print this page Share

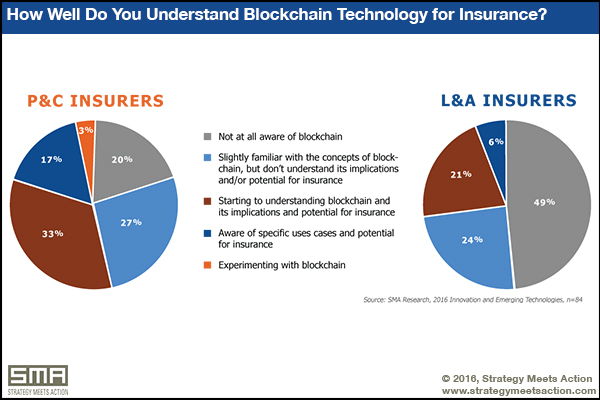

More than half of P&C insurers surveyed by insurance strategic advisory firm Strategy Meets Action (SMA) are at least aware of the implications and potential of blockchain in the industry, a new report from the company has found.

In particular, 33% of P&C insurers polled “are now starting to understand it” and 20% are “aware of specific insurance uses cases or are experimenting with the technology,” SMA said in the report, released on Thursday. Twenty-seven per cent were “slightly familiar with the concepts of blockchain, but don’t understand its implications and/or potential for insurance,” while 20% were “not at all aware of blockchain.”

In particular, 33% of P&C insurers polled “are now starting to understand it” and 20% are “aware of specific insurance uses cases or are experimenting with the technology,” SMA said in the report, released on Thursday. Twenty-seven per cent were “slightly familiar with the concepts of blockchain, but don’t understand its implications and/or potential for insurance,” while 20% were “not at all aware of blockchain.”

Boston, MA.-based SMA polled 84 P&C and life and annuity (L&A) insurers for the report, titled Blockchain in Insurance: Insurer Progress and Plans. In contrast to the P&C results, only one in four L&A insurers were aware of the technology and its potential.

Fundamentally, blockchain “provides the ability to exchange information or money directly between any two parties without the need for a trusted party as an intermediary,” SMA said in the report. “It provides a universal source of truth with full transparency and security and no need for clearinghouses or institutions to conduct transactions.” Information that is now exchanged via unsecured or semi-secured methods (such as fax, email, or overnight delivery), can be exchanged in a highly secure manner, the report said. For example, for insurance, smart contracts can enable automated triggering of contract provisions, such as claim payments.

The report, authored by SMA partner Mark Breading, found that a subset of insurers believed that blockchain has the potential to drive innovation and transformation in the industry within the next few years (by 2020). For P&C, 17% of insurers expect it to have an impact on industry transformation, while only 7% of L&A insurers see that potential in the short term.

P&C insurers see peer-to-peer insurance, microinsurance (activating/deactivating the coverage) and digital payments such as Bitcoin and Ethereum as the top opportunities for blockchain (all cited by 63% of respondents), followed by exchange of sensitive documents/information with partners/customers (53%), smart contracts (40%) and investment transactions (20%).

The report also found that P&C insurers are most actively pursuing blockchain, with 12% developing strategies, and 12% moving to pilot/experimentation status. Three per cent have deployed blockchain in production applications. Top business areas include billing, policy servicing and customer experience.

The report also found that P&C insurers are most actively pursuing blockchain, with 12% developing strategies, and 12% moving to pilot/experimentation status. Three per cent have deployed blockchain in production applications. Top business areas include billing, policy servicing and customer experience.

“Blockchain will play a vital role in the insurance industry of the future,” Breading added in a press release. “Industry awareness has been building and a variety of projects and initiatives are now underway. We expect the usage of the technology accelerate significantly after an experimentation period of two to three years. There is a wide variety of potential use cases for blockchain in insurance, ranging from applications that improve operational efficiencies to those that enable new products and new business models.”

SMA recommends that insurers learn about the basics of the technology and its potential across the business world; follow experiments and uses of blockchain in insurance and other industries; and be prepared to incorporate blockchain and other emerging technologies into mid- and long-term plans.

Last month, five insurers and reinsurers – Aegon, Allianz, Munich Re, Swiss Re and Zurich – announced the launch of the blockchain insurance industry initiative B3i, aimed at “exploring the potential of distributed ledger technologies to better serve clients through faster, more convenient and secure services.”

The five companies agreed to cooperate for a pilot project, using anonymized transaction information and quantitative data to achieve a “proof-of-concept for inter-group retrocessions by the use of blockchain technology,” Munich Re said at the time. With the feasibility study, the founding members aim to explore whether blockchain technology can be used to develop standards and processes for industry-wide usage and to “catalyze efficiency gains” in the insurance industry.

Print this page Share

Pay attention to the Insurance-Engineering Blockchain Consortium in the US. Recently Launched. Observe that the most real life contracts are too complex for simple algorithms. The Adjudicated Smart contracts keeps an individual in the loop such as an adjuster, investigator, or engineer – pre and post claim. This is important consideration that differs from banking. Banks are encumbered by KYC/AML whereas Insurance is not so the approach to blockchain will be very different. http://iebc.co